What is Schedule 1?

Schedule 1 (Form 1040) is the IRS tax form used to report two things: additional income that isn’t shown on the main Form 1040, and adjustments that lower your taxable income before deductions. Officially titled Additional Income and Adjustments to Income, Schedule 1 attaches to Form 1040, 1040-SR, or 1040-NR.

The form has two parts:

- Part I — Additional Income (lines 1–10): Income that doesn’t fit on the main 1040, like unemployment benefits, business income, freelance earnings, rental income, and prize money.

- Part II — Adjustments to Income (lines 11–26): Deductions you can take without itemizing, including educator expenses, student loan interest, half of self-employment tax, IRA contributions, and health savings account contributions.

The total from Part I flows to Form 1040, line 8. The total from Part II flows to Form 1040, line 10. Together, these numbers determine your adjusted gross income (AGI), the figure used to calculate most credits and deductions on the rest of your return.

Quick Facts about Schedule 1

- Official name: Additional Income and Adjustments to Income

- Attaches to: Form 1040, 1040-SR, or 1040-NR

- Due date: Same as your tax return; typically April 15th

- Two parts: Additional Income (Part I) and Adjustments to Income (Part II)

- What it determines: Your adjusted gross income (AGI)

Need to fill one out?

Who Needs to File Schedule 1?

You need to file Schedule 1 if you have any income that doesn’t appear directly on Form 1040, or if you want to claim any above-the-line deduction. That’s a wide net. The most common situations:

You probably need Schedule 1 if you…

- Earned freelance, gig, or 1099 income during the year

- Received unemployment compensation

- Made money from rental property, royalties, or a partnership

- Ran a small business (sole proprietor or single-member LLC)

- Had gambling winnings or won prizes/awards

- Took an early withdrawal with a penalty

- Received alimony under a pre-2019 divorce agreement

- Had digital asset (crypto) income treated as ordinary income

- Are an educator with classroom expenses

- Paid student loan interest (and qualify under the income limits)

- Contributed to a traditional IRA, HSA, SEP-IRA, or SIMPLE IRA

- Are self-employed and want to deduct half your self-employment tax or your health insurance premiums

- Made early withdrawals from CDs and were charged a penalty

- Paid alimony under a pre-2019 divorce agreement

You probably don’t need Schedule 1 if…

- Your only income is wages reported on a W-2

- You take the standard deduction and have no above-the-line adjustments

- Your interest and dividends are reported directly on Form 1099-INT or 1099-DIV (those go on the main 1040)

Worked Example: Jamie

Jamie earned $52,000 from a full-time job (reported on a W-2) and another $4,000 from weekend freelance design work (reported on a 1099-NEC). Jamie reports the $4,000 on Schedule 1, line 3 (Business income), which then flows to Form 1040, line 8. Without Schedule 1, the IRS wouldn’t see the freelance income and Jamie would be filing an incomplete return.

The Two Parts of Schedule 1

Before walking through each line, here’s the structure of the form:

| Part I — Additional Income | Part II — Adjustments to Income | |

| Lines | 1 through 10 | 11 through 26 |

| What it does | Adds income to your tax return that isn’t already on Form 1040 | Subtracts certain expenses from your income before deductions |

| Where the total goes | Form 1040, line 8 | Form 1040, line 10 |

| Effect on AGI | Increases AGI | Decreases AGI |

| Common entries | Unemployment, freelance/business income, rental income, gambling winnings | Educator expenses, student loan interest, half of SE tax, IRA deduction, HSA deduction, self-employed health insurance |

The math works in your favor. Part II adjustments reduce your AGI even if you take the standard deduction (they’re often called “above-the-line” deductions for that reason). AGI then drives eligibility for most other credits and deductions on your return, so a smaller AGI usually means a smaller tax bill.

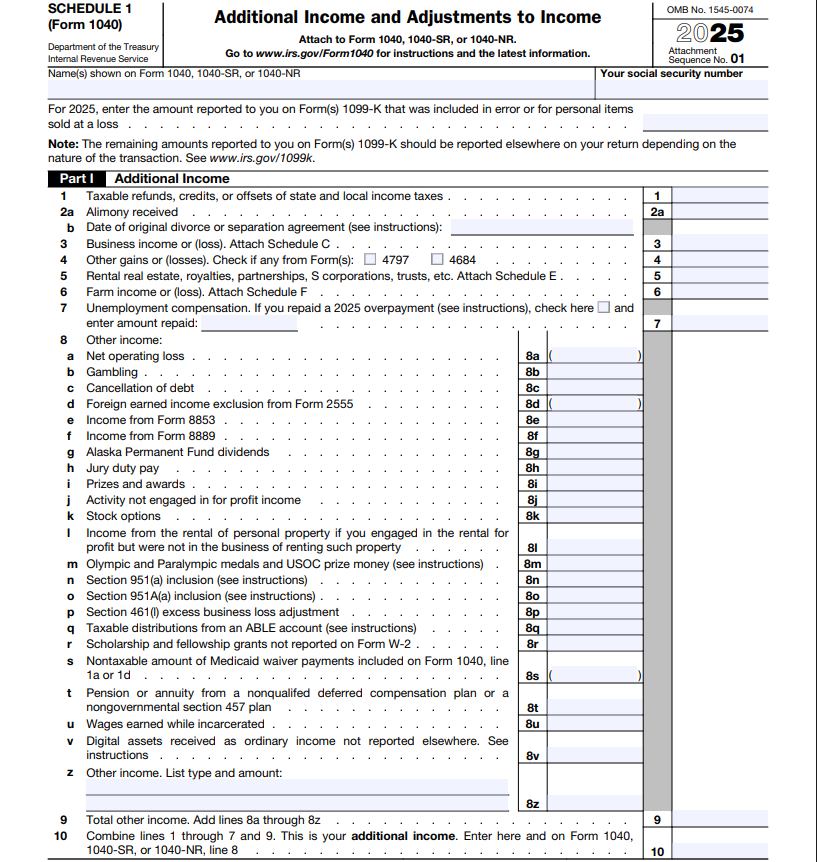

Part I: Additional Income, line-by-line

Line 1 — Taxable refunds, credits, or offsets of state and local income taxes

Report any state or local tax refund you received during the year only if you itemized deductions in a prior year and got a tax benefit from deducting state and local taxes. If you took the standard deduction last year, your state refund is not taxable and you skip this line.

Line 2a — Alimony received

Alimony you received under a divorce or separation agreement signed before January 1st, 2019. Alimony from agreements signed in 2019 or later is not taxable to the recipient and is not reported here.

Line 2b — Date of original divorce or separation agreement

Required only if you reported an amount on line 2a. Enter the date the original agreement was signed.

Line 3 — Business income or (loss)

Net profit or loss from your sole proprietorship or single-member LLC, transferred from Schedule C, line 31. If you’re a freelancer, gig worker, or self-employed professional, this is where your business income lands.

Line 4 — Other gains or (losses)

Gains or losses from the sale of business property, transferred from Form 4797. Most W-2 employees and freelancers leave this blank.

Line 5 — Rental real estate, royalties, partnerships, S corporations, trusts, etc.

Income or loss from rental property, royalties, K-1s from partnerships and S-corps, and certain trusts and estates — transferred from Schedule E.

Line 6 — Farm income or (loss)

Net farm profit or loss from Schedule F.

Line 7 — Unemployment compensation

Total unemployment benefits you received during the year, reported to you on Form 1099-G. All unemployment compensation is fully taxable at the federal level, even though some states exempt it from state tax.

Line 8 — Other income (sub-lines 8a through 8z)

A catchall for income that doesn’t fit elsewhere. Each sub-line covers a specific source:

- 8a — Net operating loss carried forward from a prior year

- 8b — Gambling winnings (from a W-2G or your own records)

- 8c — Cancellation of debt (Form 1099-C)

- 8d — Foreign earned income exclusion from Form 2555

- 8e — Income from Form 8853 (Archer MSAs and long-term care)

- 8f — Income from Form 8889 (HSA distributions used for non-medical expenses)

- 8g — Alaska Permanent Fund dividends

- 8h — Jury duty pay

- 8i — Prizes and awards (lottery, contest, etc.)

- 8j — Activity not engaged in for profit (“hobby income”)

- 8k — Stock options that aren’t statutory ISOs

- 8l — Income from rental of personal property when not in the rental business

- 8m — Olympic and Paralympic medals prize money (above an income threshold)

- 8n through 8q — Various pass-through and specialized items

- 8r — Scholarship and fellowship grants not reported on a W-2

- 8s — Nontaxable Medicaid waiver payments (when chosen to be included)

- 8t — Pension or annuity from a nonqualified deferred compensation plan

- 8u — Wages earned while incarcerated

- 8v — Digital assets received as ordinary income (from staking, mining, payment for services, etc.)

- 8z — Other income. Catch-all for anything that doesn’t fit above. Describe the type and enter the amount.

Line 9 — Total other income

Add lines 8a through 8z. This is the sum of everything in the catchall section.

Line 10 — Total additional income

Combine lines 1 through 7 and line 9. This is your total additional income: the amount that flows to Form 1040, line 8, and gets added to your wages, interest, dividends, and other primary income to determine your gross income.

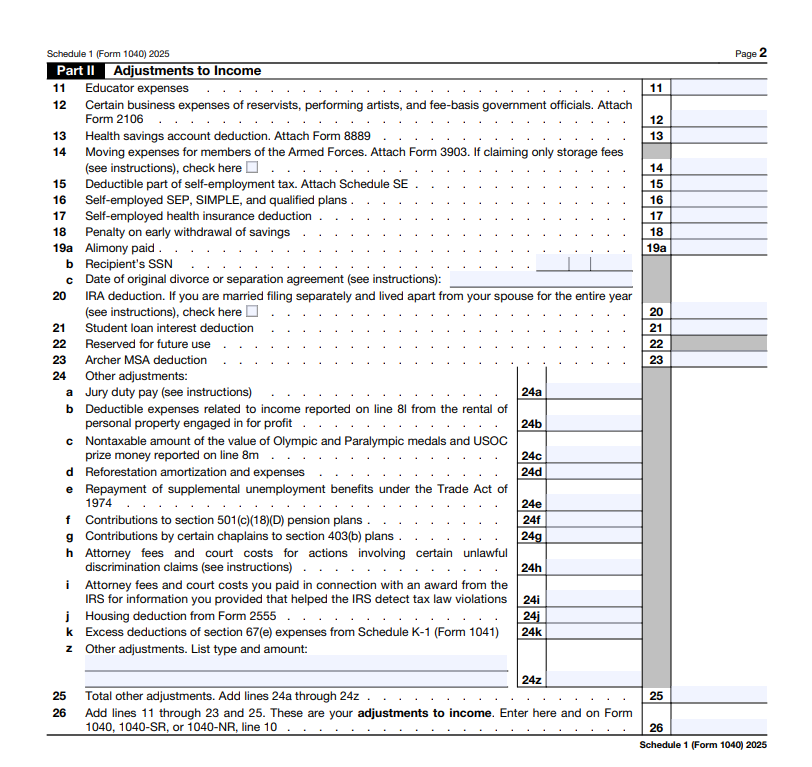

Part II: Adjustments to Income, line-by-line

Line 11 — Educator expenses

If you’re a K-12 teacher, instructor, counselor, principal, or aide who worked at least 900 hours during the year, you can deduct up to $300 in unreimbursed classroom expenses (or up to $600 if both you and your spouse qualify and file jointly).

Line 12 — Certain business expenses of reservists, performing artists, and fee-basis government officials

Specific business expenses for armed forces reservists, qualifying performing artists, and fee-basis state or local government officials. Most filers leave this blank. Requires Form 2106.

Line 13 — Health savings account (HSA) deduction

The deductible amount of your HSA contributions, transferred from Form 8889.

*Note: Only HSA contributions you made outside of payroll deduction are reported here, payroll-deducted HSA contributions are already excluded from Box 1 of your W-2.*

Line 14 — Moving expenses for members of the Armed Forces

Moving expenses are no longer deductible for most taxpayers. Active-duty military members moving on orders are the exception. Requires Form 3903.

Line 15 — Deductible part of self-employment tax

If you’re self-employed and reported SE tax on Schedule SE, you can deduct half of that tax here. This is one of the largest above-the-line deductions for freelancers and is calculated automatically by Schedule SE.

Line 16 — Self-employed SEP, SIMPLE, and qualified plans

Contributions you made to a SEP-IRA, SIMPLE IRA, or solo 401(k) as a self-employed person. These reduce your taxable income dollar for dollar (up to plan limits).

Line 17 — Self-employed health insurance deduction

If you’re self-employed and pay your own health, dental, or qualifying long-term care insurance premiums, you can deduct the full premium amount here, provided the business has a profit and you weren’t eligible for an employer-sponsored plan during that month.

Line 18 — Penalty on early withdrawal of savings

If you cashed out a CD before maturity and the bank charged you an early withdrawal penalty (shown on Form 1099-INT), deduct that penalty here.

Line 19a — Alimony paid

Alimony you paid under a divorce or separation agreement signed before January 1st, 2019. Alimony from agreements signed 2019 or later is not deductible to the payer.

- Line 19b — Recipient’s Social Security number (required if you reported on 19a)

- Line 19c — Date of the original agreement

Line 20 — IRA deduction

Traditional IRA contributions you made for the tax year, subject to income limits if you or your spouse are covered by a retirement plan at work. Roth IRA contributions are not deductible and do not go on this line.

Line 21 — Student loan interest deduction

Up to $2,500 of interest you paid on qualifying student loans during the year, subject to income phase-outs. Reported to you on Form 1098-E by your loan servicer. The deduction phases out at higher incomes; check the current year’s limits.

Line 22 — Reserved for future use

This line is currently blank and intentionally unused. The IRS reserves it for potential future use. Skip it.

Line 23 — Archer MSA deduction

Deductible Archer Medical Savings Account contributions. Most filers leave this blank since Archer MSAs were largely replaced by HSAs. Requires Form 8853.

Line 24 — Other adjustments (sub-lines 24a through 24z)

A catchall for less common above-the-line deductions:

- 24a — Jury duty pay you turned over to your employer

- 24b — Deductible expenses related to income reported on line 8l (personal property rental)

- 24c — Nontaxable Olympic/Paralympic medals and USOC prize money

- 24d — Reforestation amortization and expenses

- 24e — Repayment of supplemental unemployment benefits

- 24f — Contributions to section 501(c)(18)(D) pension plans

- 24g — Contributions by certain chaplains to section 403(b) plans

- 24h — Attorney fees and court costs for unlawful discrimination claims

- 24i — Attorney fees and court costs from IRS whistleblower awards

- 24j — Housing deduction from Form 2555 (foreign earned income exclusion)

- 24k — Excess deferrals under section 501(c)(18)(D)

- 24z — Other adjustments. Catch-all: describe the type and enter the amount.

Line 25 — Total other adjustments

Add lines 24a through 24z.

Line 26 — Total adjustments to income

Add lines 11 through 23 and line 25. This is the total amount of above-the-line deductions. It transfers directly to Form 1040, line 10, where it’s subtracted from your gross income to produce your adjusted gross income (AGI).

Generate a Compliant Schedule 1 in Minutes

The FormPros Schedule 1 generator walks you through every line with plain-English prompts, calculates totals automatically, and delivers a print-ready PDF that matches the IRS’s official format.

Create Your Schedule 1 (Form 1040)

Schedule 1 vs Schedule 1-A: Which Do You Need

Schedule 1-A is a brand-new IRS form created by the One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025. It exists alongside Schedule 1, not as a replacement. Many taxpayers will need both.

What Schedule 1 covers:

- All “additional income” sources (freelance, unemployment, rental, gambling, etc.)

- All traditional above-the-line deductions (educator expenses, student loan interest, IRA, HSA, half of SE tax, etc.)

- Permanent (has been part of Form 1040 since the 2018 tax overhaul)

What Schedule 1-A covers:

- Four temporary deductions introduced by the OBBBA:

- No tax on tips — qualified tip income (up to a cap)

- No tax on overtime — qualified overtime pay (the premium portion)

- No tax on car loan interest — interest paid on a qualifying car loan

- Temporary (applies only to tax years 2025 through 2028)

- Available with the standard deduction — you don’t have to itemize to claim them

Quick Decision Guide

| Your Situation | Schedule 1? | Schedule 1-A? |

| W-2 worker with no extra income or deductions | No | No |

| Freelancer, gig worker, or rental property owner | Yes | Maybe (if you have tips or claim a senior deduction) |

| Teacher claiming the educator expense deduction | Yes | No |

| Student loan borrower | Yes | No |

| Tipped worker (server, bartender, hairdresser) | Maybe | Yes (qualified tips) |

| Overtime-eligible hourly worker | Maybe | Yes (qualified overtime) |

| Senior (65+) taking the standard deduction | Maybe | Yes (enhanced deduction) |

| Bought a car with a qualifying loan in 2025 | Maybe | Yes (car loan interest) |

Where each total flows on Form 1040:

- Schedule 1 Part I total → Form 1040, line 8 (adds to your income)

- Schedule 1 Part II total → Form 1040, line 10 (reduces your income)

- Schedule 1-A total → Form 1040, line 13b (further reduces your taxable income)

Want a deeper dive on Schedule 1-A? Read our complete guide: New Schedule 1-A Tax Form: What It Is and Who Needs to File It

Schedule 1 vs Schedule 2 vs Schedule 3

The IRS uses three numbered schedules to extend Form 1040 beyond its main lines. Each does something different:

| Schedule | What It Covers | Where The Total Goes On 1040 |

| Schedule 1 | Additional income & above-the-line deductions | Lines 8 (income) and 10 (adjustments) |

| Schedule 2 | Additional taxes (AMT, self-employment tax, additional Medicare, etc.) | Lines 17 and 23 |

| Schedule 3 | Additional credits and payments (foreign tax credit, child & dependent care credit, education credits, etc.) | Lines 20 and 31 |

| Schedule 1-A | Four temporary OBBBA deductions (tips, overtime, car loan interest, senior) | Line 13b |

You can attach any combination of these to your Form 1040 as they’re not mutually exclusive. Most filers who need Schedule 1 also need Schedule 2 or Schedule 3.

Common Schedule 1 Scenarios

1) Side-hustle freelancer

Maria earns $58,000 at her day job and another $7,200 driving rideshare on weekends. She also paid $1,400 in student loan interest.

- Line 3: $7,200 business income (after Schedule C expenses)

- Line 15: ~$510 (half of self-employment tax)

- Line 21: $1,400 student loan interest

Net effect: Her AGI rises by ~$5,290 from the rideshare income but is reduced by the SE tax and student loan deductions.

2) Teacher with student loans

David is a high school teacher earning $54,000 in W-2 wages. He spent $280 on classroom supplies and paid $1,800 in student loan interest.

- Part I: Empty (no additional income)

- Line 11: $280 educator expense deduction

- Line 21: $1,800 student loan interest deduction

- Line 26 total: $2,080 reduction to AGI; even though David takes the standard deduction.

3) Unemployment recipient who returned to work

Priya received $9,400 in unemployment in early 2025 (Form 1099-G), then started a new job in May earning $46,000.

- Line 7: $9,400 unemployment compensation

- Part II: Empty

Net effect: $9,400 added to her gross income via Schedule 1.

4) Rental property owner with self-employment

Marcus runs a small consulting LLC ($28,000 net) and owns a rental property ($4,200 net rental income).

- Line 3: $28,000 (Schedule C → Schedule 1)

- Line 5: $4,200 (Schedule E → Schedule 1)

- Line 15: ~$1,980 (half of SE tax)

- Line 16: $5,000 SEP-IRA contribution

- Line 17: $4,800 self-employed health insurance premiums

5) Tipped worker (also needs Schedule 1-A)

Riley is a server earning $32,000 in W-2 wages (including reported tips) and $1,800 from a one-off freelance photography gig.

- Schedule 1, Line 3: $1,800 freelance income

- Schedule 1-A: Riley files this separately to claim the new “no tax on tips” deduction for the qualifying tip portion of her wages.

Common Mistakes on Schedule 1

Not filing Schedule 1 at all when it’s required.

— Most common error. People assume “I just have a regular job, I don’t need extra forms.” Then they miss the educator expense deduction, the student loan interest deduction, or — more seriously — fail to report a 1099 they received.

Reporting freelance income directly on Form 1040 instead of Schedule 1.

— To clarify, freelance income flows to Schedule 1, line 3; specifically, by way of Schedule C. As a result, reporting the gross amount directly on Form 1040 not only misses the Schedule C deductions but also triggers IRS matching errors.

Missing the alimony cutoff.

— Alimony from agreements signed in 2019 or later is not taxable to the recipient and not deductible by the payer. Putting post-2018 alimony on lines 2a or 19a is a common error.

Confusing Roth and traditional IRA contributions.

— Specifically, only traditional IRA contributions go on line 20. Roth contributions, by contrast, are not deductible. Even so, people sometimes claim both and that’s an error.

Skipping Schedule 1-A when it applies.

— Now that Schedule 1-A exists for tips, overtime, car loan interest, and the enhanced senior deduction, many filers will miss those temporary deductions if they only file Schedule 1.

Forgetting the half-of-SE-tax deduction.

— If you owe self-employment tax (Schedule SE), you almost always also get to deduct half of it on Schedule 1, line 15. This is automatic in tax software but easy to miss when filing by hand.

Reporting state tax refunds when you took the standard deduction.

— State refunds are only taxable if you itemized in the year you paid the original state taxes. If you took the standard deduction, your state refund isn’t taxable and shouldn’t appear on line 1.

Double-counting payroll-deducted HSA contributions.

— Importantly, HSA contributions made through payroll deduction are already excluded from Box 1 wages on your W-2. As a result, don’t deduct them again on line 13; otherwise, that’s double-dipping.

Forgetting to attach supporting schedules.

— Schedule 1 references several other forms: Schedule C (line 3), Schedule E (line 5), Schedule F (line 6), Schedule SE (line 15), Form 2106, Form 3903, Form 8889, etc. Skipping the supporting form is a common e-file rejection cause.

How to File Schedule 1

Step 1 — Gather Your Documents

Pull together W-2s, all 1099s (NEC, MISC, K, INT, DIV, R, G), Schedule K-1s, Form 1098-E (student loan interest), Form 1098 (mortgage interest, if relevant), records of educator expenses, and HSA/IRA contribution statements.

Step 2 — Complete Supporting Schedules First

Schedule 1 references several other schedules. If you have business income, complete Schedule C first. Rental income? Schedule E. Self-employment tax? Schedule SE. Those totals feed into Schedule 1.

Step 3 — Fill in Part I (Additional Income)

Work line by line through 1 through 8z. Sum lines 8a–8z to line 9. Combine lines 1–7 plus 9 to get line 10.

Step 4 — Fill in Part II (Adjustments to Income)

Work line by line through 11 through 24z. Sum lines 24a–24z to line 25. Add lines 11–23 plus 25 to get line 26.

Step 5 — Transfer Totals to Form 1040

- Line 10 of Schedule 1 → Form 1040, line 8

- Line 26 of Schedule 1 → Form 1040, line 10

Step 6 — Attach Schedule 1 to Your Return

File electronically (most tax software handles attachment automatically) or include the printed Schedule 1 behind your Form 1040 if filing by mail.

Filing Deadlines and Extensions

| Date | What’s Due |

| April 15th | Federal tax return (Form 1040 + all attached schedules including Schedule 1) |

| April 15th | Any taxes owed (even if you file an extension) |

| October 15th | Extended filing deadline (if you filed Form 4868) |

If April 15th falls on a weekend or federal holiday, the deadline moves to the next business day. An extension to file is not an extension to pay; interest and penalties accrue on unpaid tax from April 15th onward, regardless of whether you’ve extended your filing.

Create Schedule 1 (Form 1040) Now

Form 1040 (Schedule 1) FAQs

-

What is Schedule 1 used for?

First, Schedule 1 reports two things: namely, additional income that isn't on Form 1040 (such as freelance income or unemployment), as well as above-the-line deductions (for example, student loan interest or educator expenses). From there, the totals flow to Form 1040, lines 8 and 10.

-

Do I need Schedule 1 if I only have a W-2?

Generally speaking, probably not unless, of course, you want to claim an above-the-line deduction such as student loan interest, educator expenses, or HSA contributions. In that case, however, you'll file Schedule 1 even with W-2-only income.

-

Where does Schedule 1 line 10 go on Form 1040?

Once completed, line 10 of Schedule 1 (that is, your total additional income) then transfers to Form 1040, line 8.

-

Where does Schedule 1 line 26 go on Form 1040?

Similarly, line 26 of Schedule 1 (that is, your total adjustments to income) transfers to Form 1040, line 10. From there, it's then subtracted from your gross income to compute your AGI.

-

Can I file Schedule 1 electronically?

Yes. In fact, all major tax software automatically attaches Schedule 1 whenever you report income or deductions that require it.

-

What’s the difference between Schedule 1 and Schedule 1-A?

On the one hand, Schedule 1 covers additional income and traditional above-the-line deductions. On the other hand, Schedule 1-A is a brand-new form (specifically, for tax years 2025–2028) that covers four temporary deductions: namely, tips, overtime, car loan interest, and an enhanced senior deduction.

-

Do I need Schedule 1 if I’m self-employed?

Yes. In fact, self-employment income flows from Schedule C to Schedule 1, line 3. Beyond that, you'll also use Schedule 1 to deduct half your self-employment tax (specifically, on line 15) and self-employed health insurance premiums (line 17 in particular).

-

Can married couples file one Schedule 1 together?

Yes. Specifically, when you file jointly, both spouses' additional income and adjustments are reported together on a single Schedule 1.

-

What if I forget to attach Schedule 1?

If that happens, the IRS may delay your refund or, alternatively, send a notice asking for the missing schedule. Fortunately, you can correct the omission by filing an amended return, specifically, Form 1040-X.

-

Are adjustments on Schedule 1 the same as itemized deductions?

No. Rather, adjustments on Schedule 1 (Part II) are known as 'above-the-line' deductions, meaning they reduce your AGI before you take the standard or itemized deduction. As a result, you can claim them whether you itemize or take the standard deduction.

-

Does Schedule 1 apply to recent graduates and students?

Often, yes. For instance, recent graduates paying student loan interest will specifically use line 21. Likewise, students with taxable scholarships, freelance income, or 1099 work typically file Schedule 1 as well.

-

Do I need Schedule 1 for cryptocurrency income?

Yes, in many cases. For example, crypto received as ordinary income (such as staking rewards, mining income, or payment for services) is reported on Schedule 1, line 8v.

-

Where do I send Schedule 1?

Specifically, Schedule 1 is filed together with your Form 1040 that is, through the same address or e-file pathway you use for the main return. As a result, there's no separate filing required.