Get Your Printable W-2 Form in 3 Easy Steps

-1-

Fill W2 form online: enter employer and employee details.

-2-

Get a free consultation to save tax (optional).

-3-

Download your printable W-2 Form.

What is a W-2 Form?

A W-2, officially called the Wage and Tax Statement, is a tax form employers send to every employee who earned at least $600 during the year. It reports the employee’s total wages, tips, and other compensation for the year, along with the federal, state, Social Security, and Medicare taxes the employer withheld from their paychecks.

Employers must send each employee a W-2 by January 31st following the end of the tax year, and file a copy with the Social Security Administration (SSA) by the same date. Employees use their W-2 to file their federal and state income tax returns; the IRS requires it to verify reported income.

Employers issue the W-2 to their employees. Independent contractors, freelancers, and gig workers receive a Form 1099-NEC instead (we cover the difference in Section 9 below).

Quick Facts:

- Who sends it: Your employer

- Who gets it: Any employee who earned $600+ in the tax year

- When you get it: By January 31 of the year following the tax year

- What it’s for: Filing your federal and state tax returns

- IRS name: Form W-2, Wage and Tax Statement

Who Gets a W-2?

You should receive a W-2 if you were an employee at any point during the tax year and earned $600 or more. That includes part-time, seasonal, and temporary workers; anyone whose employer withheld federal, Social Security, or Medicare taxes from their pay.

You will not receive a W-2 if:

- You were an independent contractor (you’ll get a 1099-NEC instead)

- You were self-employed or a sole proprietor (you report income on Schedule C)

- You worked for cash “off the books” (though you’re still legally required to report that income)

If you worked multiple jobs during the year, you should receive a separate W-2 from each employer. All W-2s from that year go on the same tax return.

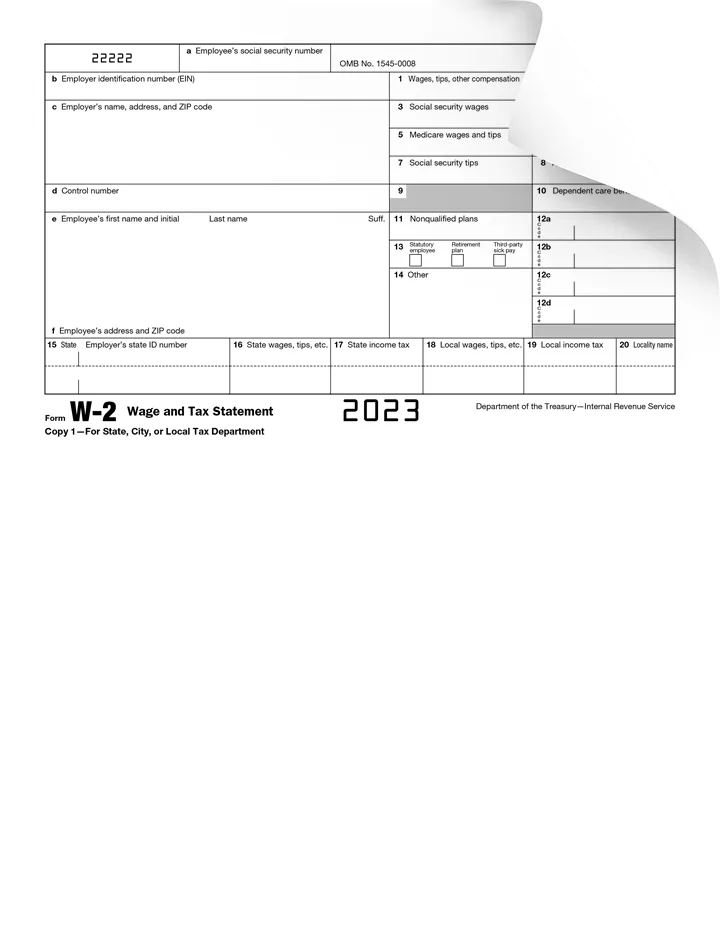

How to Read Your W-2 (Box-by-Box)

Every W-2 has three parts:

- Employee/Employer Identification: (Boxes a–f)

- Earnings and Withholdings: (Boxes 1–14)

- State and Local Tax Information: (Boxes 15–20)

Here’s what each one means.

Identification Boxes:

Box a — Employee’s Social Security Number (SSN): Your SSN. If this is wrong, ask your employer to issue a corrected W-2 (Form W-2c) immediately, the IRS matches this against your return.

Box b — Employer Identification Number (EIN): Your employer’s 9-digit federal tax ID. You’ll need this if you’re filing your taxes without a W-2 and have to reference your employer.

Box c — Employer’s Name, Address, and ZIP code: Straightforward. Verify this matches the company you worked for.

Box d — Control Number: An optional box some employers use for internal payroll tracking. Box d is often blank, and that’s fine — you don’t need it to file your taxes.

Box e — Employee’s Name: Your full legal name, exactly as it appears on your Social Security card. Any mismatch can delay your return.

Box f — Employee’s Address: Where your W-2 was mailed. Update with your employer if this is outdated.

Earnings and Withholding Boxes (1-14):

Box 1 — Wages, tips, other compensation: Your total taxable wages for federal income tax. This is usually less than your gross pay because it excludes pre-tax deductions like 401(k) contributions and pre-tax health insurance. This is the number that goes on line 1a of your Form 1040.

Box 2 — Federal income tax withheld: The total federal income tax your employer withheld from your paychecks and sent to the IRS on your behalf. If Box 2 is more than your tax liability, you get a refund.

Box 3 — Social Security wages: Wages subject to Social Security tax, which is capped each year. For tax year 2025, the cap is $176,100. Wages above that cap aren’t subject to Social Security tax.

Box 4 — Social Security tax withheld: 6.2% of Box 3. If your employer withheld more than the Social Security maximum, request a refund or credit it on your 1040.

Box 5 — Medicare wages and tips: Wages subject to Medicare tax. Unlike Box 3, there’s no cap on Medicare wages; all of your wages are subject to Medicare tax.

Box 6 — Medicare tax withheld: 1.45% of Box 5 for most employees. Higher earners (over $200K) pay an additional 0.9% Medicare surtax.

Box 7 — Social Security tips: Tips you reported to your employer during the year. Most employees outside food service and hospitality will see $0 here.

Box 8 — Allocated tips: Tips your employer allocated to you. Also typically $0 unless you work in a large food/beverage establishment.

Box 9 — Blank: This box is intentionally unused on current W-2s. Leave it alone.

Box 10 — Dependent care benefits: Amounts your employer paid or reimbursed for dependent care (up to a limit, the rest is taxable). Relates to Form 2441 if you have dependent care expenses.

Box 11 — Nonqualified plans: Distributions from a nonqualified deferred compensation plan. If you don’t know what that is, this box is probably $0 for you.

Box 12 — Codes and amounts (see full table below): The most commonly asked-about box. Your employer enters letter codes here that represent specific types of compensation or deductions: things like 401(k) contributions (code D), Roth 401(k) (code AA), or the cost of employer-sponsored health coverage (code DD). A full breakdown of every Box 12 code follows in the next section.

Box 13 — Checkboxes: Three checkboxes: Statutory employee, Retirement plan, and Third-party sick pay. If “Retirement plan” is checked, your IRA deduction may be limited depending on your income.

Box 14 — Other (see full explanation below): A catch-all box for items that don’t fit elsewhere: state disability insurance, union dues, uniform reimbursements, educational assistance, and dozens of other employer-specific items. Because Box 14 is unstructured, codes here vary by employer and aren’t standardized by the IRS.

State and Local Tax Boxes (15-20):

Box 15 — State and state ID: Your employer’s state and state tax ID.

Box 16 — State wages, tips, etc.: Wages subject to state income tax; may differ from Box 1 based on state rules.

Box 17 — State income tax: State income tax withheld.

Box 18 — Local wages, tips, etc.: Wages subject to local (city, county, school district) tax, if applicable.

Box 19 — Local income tax: Local tax withheld.

Box 20 — Locality name: The locality imposing the local tax.

W-2 Box 12 Codes – The Complete Reference

Box 12 uses letter codes to identify specific types of compensation, deductions, and benefits. Each code is paired with a dollar amount. You can have up to four Box 12 items on a single W-2 (12a, 12b, 12c, 12d). Here’s every current Box 12 code and what it means:

| Code | Meaning | Tax Treatment |

| A | Uncollected Social Security tax on tips | Reported on Schedule 2 |

| B | Uncollected Medicare tax on tips | Reported on Schedule 2 |

| C | Taxable cost of group-term life insurance over $50,000 | Included in Box 1 |

| D | 401(k) plan contributions | Pre-tax; reduces Box 1 |

| E | 403(b) plan contributions | Pre-tax |

| F | 408(k)(6) SEP plan contributions | Pre-tax |

| G | 457(b) plan contributions | Pre-tax |

| H | 501(c)(18)(D) plan contributions | Pre-tax |

| J | Non-taxable sick pay | Not included in Box 1 |

| K | 20% excise tax on excess golden parachute payments | |

| L | Substantiated employee business expense reimbursements | |

| M | Uncollected Social Security tax on group-term life insurance | |

| N | Uncollected Medicare tax on group-term life insurance | |

| P | Excludable moving expense reimbursements (armed forces only) | |

| Q | Nontaxable combat pay | |

| R | Employer contributions to Archer MSA | |

| S | SIMPLE IRA contributions | Pre-tax |

| T | Adoption benefits | |

| V | Income from exercise of nonstatutory stock options | Included in Box 1 |

| W | Employer HSA contributions | Pre-tax |

| Y | Deferrals under 409A nonqualified deferred compensation | |

| Z | Income under 409A on a nonqualified deferred compensation plan | |

| AA | Roth 401(k) contributions | After-tax |

| BB | Roth 403(b) contributions | After-tax |

| DD | *Cost of employer-sponsored health coverage* | *Informational only — not taxable* |

| EE | Roth 457(b) contributions | After-tax |

| FF | Permitted benefits under QSEHRA | |

| GG | Income from qualified equity grants under 83(i) | |

| HH | Aggregate deferrals under 83(i) elections |

*Code DD is the most searched Box 12 code and the one that confuses employees most. It shows the total cost of your employer’s health insurance plan (both your contribution and the employer’s). Code DD is informational only (it does not increase your taxable income).*

W-2 Box 14: What the Codes Mean

Box 14 is a catch-all; unlike Box 12, there’s no standardized list of codes. The IRS lets employers use Box 14 for any item they want to report that doesn’t fit elsewhere. Common Box 14 entries include:

- CA-SDI, NY-SDI, NJ-SDI, etc. — State Disability Insurance withheld (deductible on Schedule A if you itemize)

- SUI — State Unemployment Insurance

- FLI — Family Leave Insurance

- UNION or DUES — Union dues (no longer federally deductible for most employees)

- RR — Railroad retirement amounts

- K — Pre-tax dental, vision, or other benefits

- Educ — Employer-provided educational assistance above the excludable amount

- 125 — Section 125 cafeteria plan contributions

- 414(h) — Certain government employee retirement contributions

- Overtime — In some states, Box 14 is used to separately report overtime wages

Because Box 14 isn’t standardized, if you see a code on yours you don’t recognize, the fastest way to find out what it means is to ask your employer’s payroll department. Most tax software will either prompt you through common codes or skip Box 14 entirely for codes it doesn’t know, and that’s usually fine, because items in Box 14 that affect your taxes are already captured elsewhere (like state SDI being deductible if you itemize).

How to Get Your W-2 (For Employees)

Your employer is legally required to send you a W-2 by January 31st. Most employers deliver it one of three ways: mailed to your address on file, handed out at work, or posted to an online payroll portal (ADP, Workday, Paychex, etc.). If January 31st has passed and you don’t have your W-2, follow these steps in order:

1. Check your employer’s online payroll portal first –

Most mid-size and large employers post W-2s digitally before they mail them. Common portals include ADP Workforce Now, Workday, Paychex Flex, Gusto, and iSolved. Log in to the same system where you view your paystubs.

2. Contact your employer or former employer directly –

If you can’t find the portal or you’ve changed jobs, call the HR or payroll department. Provide:

- Your full name as it appeared on your paychecks

- Your Social Security number (last 4 digits usually enough)

- Your current mailing address

- Your dates of employment

Employers are required to provide a replacement W-2 if you lost or never received yours. There is no fee for a reissued W-2.

3. Contact the IRS (after February 14th) –

If you still don’t have your W-2 by February 14th, call the IRS at 1-800-829-1040. You’ll need:

- Your employer’s name, address, and EIN

- Your dates of employment

- An estimate of your wages and federal tax withheld (use your last paystub)

The IRS will contact your employer and send you Form 4852, a substitute for your W-2.

4. File with a substitute W-2 if necessary –

If your filing deadline is approaching and you still don’t have your W-2, you can file using Form 4852 (Substitute for W-2) based on your estimates. If your actual W-2 arrives later and the numbers differ, you’ll need to file an amended return using Form 1040-X.

5. Access prior-year W-2s through the IRS –

For W-2s from previous years, use the IRS Get Transcript tool. Request a “Wage and Income Transcript”; it will show the data from W-2s (and other wage forms) the IRS received from employers for the past 10 years.

What if your employer refuses to send your W-2? Employers who fail to furnish a W-2 can be penalized up to $680 per form (2026 penalty amount), with higher penalties for intentional failure. Report the issue to the IRS after February 14th using the steps above.

How to Create and Issue W-2’s (For Employers)

If you’re an employer, you must issue a W-2 to every employee you paid $600 or more during the year — and file Copy A with the Social Security Administration by January 31st. This section walks through the process.

Employer W-2 Checklist:

- Gather each employee’s information — full legal name, Social Security number, and mailing address.

- Pull their year-to-date payroll data — total wages (Box 1), federal withholding (Box 2), Social Security and Medicare wages and taxes (Boxes 3–6), state and local wages and taxes, and any Box 12 items (retirement contributions, health insurance cost, HSA, etc.).

- Generate each W-2 — you can buy official red-ink forms from an office supply store or online, or use payroll software or a W-2 generator. Copy A must be scannable by IRS equipment.

- Distribute Copies B, C, and 2 to employees by January 31st (mail or electronic if the employee consented).

- File Copy A + Form W-3 with the SSA by January 31st. The SSA strongly encourages electronic filing through Business Services Online (BSO).

- File state copies with your state tax agency — deadlines vary by state.

- Retain your copies for four years for audit purposes.

Generate Compliant W-2s in Minutes

The FormPros W-2 generator builds an IRS-compliant W-2 in under two minutes. You enter employer and employee details, wages, and withholdings. We auto-calculate the tax fields and deliver a ready-to-distribute PDF.

*All forms on this site are for informational purposes only and cannot be used to file taxes. The IRS uses optical character recognition equipment that requires specific formatting personal printers cannot replicate. To file, you can order official forms at IRS.gov/OrderForms, file electronically at IRS.gov/FIRE or IRS.gov/AIR, or consult a qualified tax professional.*

W-2 Deadlines and Penalties

January 31st is the single most important W-2 date. Both the employee distribution and the SSA filing must be done by January 31st (this has been the rule since 2016).

| Deadline | Requirement |

| January 31st | Distribute W-2s to employees (Copies B, C, 2) |

| January 31st | File Copy A + Form W-3 with the Social Security Administration |

| January 31st | File state W-2 copies (most states; check yours) |

| February 14th | Earliest date an employee can contact the IRS about a missing W-2 |

| April 15th | Federal tax filing deadline for employees using the W-2 |

*If January 31st falls on a weekend or federal holiday, the deadline moves to the next business day.*

Penalties for late or incorrect W-2s

| How late | Penalty per form |

| Filed within 30 days of deadline | $60 |

| Filed by August 1st | $130 |

| Filed after August 1st (or not at all) | $340 |

| Intentional disregard | $680+ per form, no cap |

W-2 vs W-4 vs W-9 vs 1099: How They Differ

These four forms get confused constantly. Here’s how they relate:

| Form | Who fills it out | Who gets it | What it’s for |

| W-2 | Employer | Employee | Reports an employee’s annual wages and tax withholdings. |

| W-4 | Employee | Employer | Tells the employer how much federal tax to withhold from each paycheck. |

| W-9 | Independent contractor | Payer | Provides contractor’s taxpayer ID so the payer can issue a 1099. |

| 1099-NEC | Payer | Contractor | Reports a contractor’s annual earnings (equivalent of a W-2 for contractors). |

The simplest way to think about it:

– W-2 and W-4 both involve employees. The W-4 comes first (when hired) and tells the employer what to withhold; the W-2 comes at year-end and reports what was actually withheld.

– W-9 and 1099 both involve independent contractors. The W-9 comes first (when engaged) and provides the contractor’s info; the 1099-NEC comes at year-end and reports what was paid.

If you’re getting a W-2, you’re an employee. If you’re getting a 1099-NEC, you’re an independent contractor.

Common W-2 Mistakes to Avoid

1) Using a form from the wrong tax year: tax rates and reporting requirements change annually.

2) Incorrect employee name or SSN: must match the Social Security card exactly.

3) Including titles or nicknames in the name field: no “Dr.”, “Mrs.”, “Jr.” unless legally part of the name.

4) Missing the January 31st deadline: late filing penalties start at $60 per form.

5) Handwritten or non-scannable forms: the IRS requires machine-readable formatting.

6) Wrong or missing EIN: the EIN must match what the IRS has on file.

7) Leaving Box 13 (Retirement plan) unchecked when it should be checked: affects the employee’s IRA deduction eligibility.

State-Specific W-2 Requirements

While the federal W-2 process is uniform, state filing requirements vary significantly. Some states (like California, New York, Illinois, and Pennsylvania) require employers to file state W-2 copies directly with the state tax agency. Others participate in the IRS Combined Federal/State Filing Program, meaning the SSA forwards state data automatically.

A few states (including Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, and Wyoming) have no state income tax and therefore no state W-2 filing requirement. Before filing W-2s with your state, check:

- Whether your state requires a separate W-2 filing.

- The state’s filing deadline (usually January 31st, but some differ).

- Whether the state accepts paper or requires electronic filing.

- Any state-specific reconciliation forms (California DE 9C, Illinois UI-3/40, New York NYS-45, etc.)

Form W-2 FAQs

-

What is a W-2 form used for?

A W-2 reports an employee’s annual wages and the federal, state, Social Security, and Medicare taxes withheld by their employer. Employees use it to file their federal and state income tax returns.

-

Who gets a W-2 form?

Any employee who earned at least $600 from an employer during the tax year receives a W-2. Independent contractors and freelancers receive a 1099-NEC instead.

-

When should I receive my W-2?

Employers must send W-2s by January 31st. If you haven’t received yours by mid-February, check your employer’s payroll portal, then contact HR.

-

How can I get my W-2 online for free?

Log in to your employer’s payroll portal (ADP, Workday, Paychex, Gusto, etc.) — most employers post W-2s online before mailing. For prior years, use the IRS Get Transcript tool to request a Wage and Income Transcript.

-

What do I do if my employer won’t give me a W-2?

After February 14th, call the IRS at 1-800-829-1040. The IRS will contact your employer and send you Form 4852, a substitute W-2. Employers face penalties starting at $680 per form for failing to issue W-2s.

-

Can I print my own W-2?

Employees cannot create their own W-2s (only the employer can issue one). Employers can generate and print W-2s using official forms or a W-2 generator.

-

What’s the difference between a W-2 and a W-4?

Employees fill out a W-4 when hired to tell the employer how much tax to withhold. The employer issues a W-2 at year-end summarizing what was actually paid and withheld.

-

What’s the difference between a W-2 and a 1099?

A W-2 is for employees with taxes withheld by the employer. A 1099-NEC is for independent contractors who pay their own taxes.

-

Is Box 1 or Box 3 my “gross income”?

Neither is your true gross income.

Box 1 is taxable wages for federal income tax (pre-tax deductions like 401(k) are subtracted).

Box 3 is Social Security wages.

Your actual gross pay is usually higher than both, which is why your paystub shows the full gross.

-

What is Adjusted Gross Income (AGI) on a W-2?

AGI isn’t on your W-2. It’s calculated on your Form 1040 by taking your total income (including Box 1 of your W-2) and subtracting above-the-line deductions like student loan interest and HSA contributions.

-

What if the information on my W-2 is wrong?

Ask your employer to issue a Form W-2c (Corrected Wage and Tax Statement). Don’t wait, file early enough that you can use the corrected form on your return.

-

How long should I keep my W-2?

Keep W-2s for at least three years from the date you filed your return (seven years if you claimed a loss from worthless securities or bad debt). More on tax record retention