What is the official name of Form 1099-C and what is its purpose?

The official name of Form 1099-C is “Cancellation of Debt.” Its purpose is to report the cancellation, discharge, or forgiveness of a debt amounting to $600 or more by a creditor. This form is used to enable both the Internal Revenue Service (IRS) and the debtor to be aware of the forgiven debt, which is generally treated as taxable income. It ensures that the debtor accurately reports this information on their tax return for compliance with federal tax laws.

Why is Form 1099-C important?

Form 1099-C is crucial as it provides both the IRS and taxpayers with essential information about cancelled, discharged, or forgiven debts over $600. This form ensures tax compliance by necessitating that the forgiven debt is reported as taxable income by the debtor. Its accurate completion allows taxpayers to adhere to federal tax laws, preventing potential errors in tax reporting and avoiding issues such as unexpected tax liabilities or penalties for underreporting income. By furnishing details such as the amount of debt forgiven and the identity of the debtor and creditor, it plays a key role in the transparency and traceability of financial transactions related to debt forgiveness.

Who is required to submit a Form 1099-C?

Creditors who have canceled, discharged, or forgiven a debt of $600 or more are required to submit Form 1099-C, Cancellation of Debt, to the Internal Revenue Service and to the debtor. This includes financial institutions, credit card companies, or any other entities that forgive debts as part of their business practices.

What are the specific steps to obtain and correctly complete Form 1099-C?

To obtain and correctly complete Form 1099-C, Cancellation of Debt, you should first download the form from the IRS website or acquire it from an IRS office. It’s crucial that the creditor, who is reporting the cancellation of debt, uses the correct version of the form for the corresponding tax year.

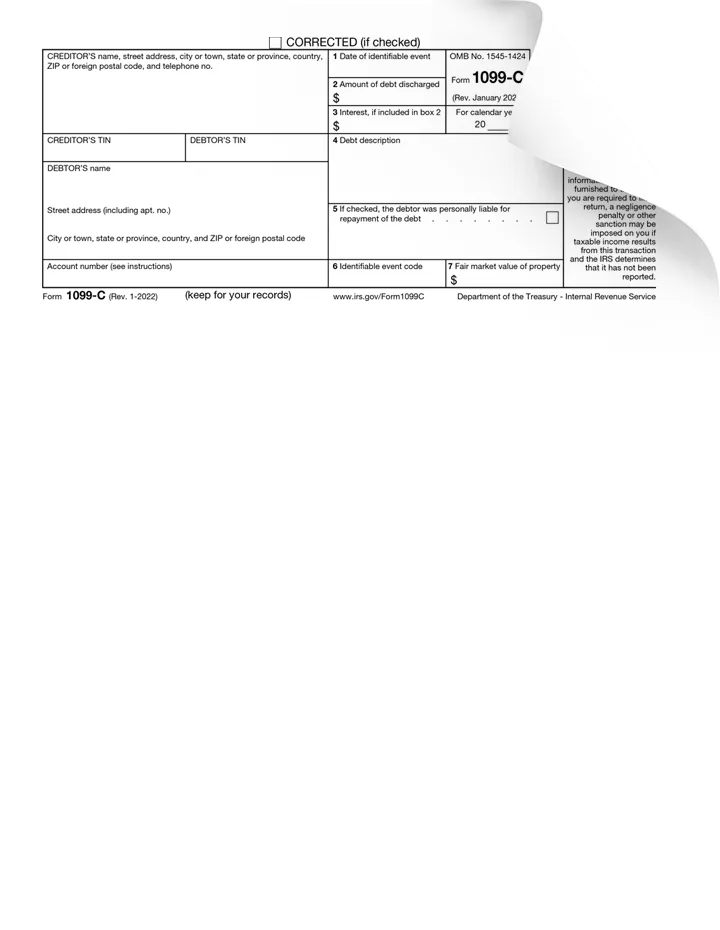

When filling out Form 1099-C, the following information must be provided: the name, address, and taxpayer identification number (TIN, typically a Social Security Number or an Employer Identification Number) of both the lender (creditor) and the debtor. The form must also include the account number to ensure proper identification of the debt.

Enter the date of the identifiable event which led to the debt cancellation in the appropriate field. This is the date on which the debt was forgiven, settled, or deemed uncollectible. The amount of the canceled debt that should be reported in the “Amount of debt discharged” box must be $600 or more. If applicable, include any interest that was part of the forgiven debt in this amount.

If the debtor was personally liable for the debt, this should be indicated by marking the appropriate checkbox. This determines whether the debt is recourse or non-recourse which affects the insolvency calculations of the debtor, if applicable.

After completing the form, it must be provided to the debtor by January 31st following the calendar year in which the debt was canceled. A copy of the form must also be submitted to the IRS by the end of February (if filing by paper) or by the end of March (if filing electronically). Ensure that all provided information matches records and that appropriate copies are kept for record-keeping. Additionally, it’s advised to consult with a tax professional or refer to IRS instructions to ensure compliance with specific filing requirements and avoid any errors during the completion process.

When and how often do you need to file Form 1099-C, and are there any associated deadlines?

Form 1099-C is typically required to be filed by creditors whenever they forgive a debt exceeding $600 during the tax year. The completed form must be sent to the IRS and to the debtor by January 31st of the year following the cancellation of the debt. This deadline ensures that debtors receive the form in time to include the information in their tax returns for that year. There is no routine requirement for debtors to submit this form themselves, as it is the responsibility of the creditor to file and distribute it accordingly.

Are there any consequences for late submission of Form 1099-C?

Yes, there are consequences for late submission of Form 1099-C. The IRS may impose penalties on the creditor for failing to timely file the form. These penalties vary based on how late the form is filed and can accumulate for each form not submitted on time. The penalties can range from $50 to $280 per form, depending on the delay’s extent, up to a maximum of $1,130,500 per year for small businesses and $3,426,000 for larger entities. Additionally, intentional disregard for filing requirements can result in even higher penalties.

Can you list the key components or sections that Form 1099-C comprises?

Form 1099-C comprises several key components that include:

- The identities of both the creditor and the debtor

- The principal amount of the debt canceled

- Any interest that was included in the forgiven debt

- The date on which the debt was canceled

- A checkbox to indicate if the debtor was personally liable for the debt

Additionally, there is a section for pertinent descriptions or codes that explain the reason for the debt cancellation. These elements together provide a comprehensive snapshot of the financial event for tax reporting purposes.

What documents should I have on hand to help me complete these sections accurately?

To accurately complete Form 1099-C, have these documents readily available:

- The original loan agreement or debt contract to verify the initial amount of debt and the terms of the agreement.

- Any correspondence from the creditor regarding the cancellation of the debt, which typically includes the amount forgiven and relevant dates.

- Account statements from the creditor showing the balance of the debt before and after cancellation, which will help verify the amount reported on Form 1099-C.

- Financial records relating to any payments made on the debt, which might include bank statements or receipts.

- Legal documents pertaining to the cancellation of the debt if it was discharged through legal proceedings, such as bankruptcy court documents.

- Documentation indicating whether you were personally liable for the debt repayment, which could include terms from the original debt agreement or a court ruling.

A case study showcasing the importance of Form 1099-C.

Consider the scenario of Sarah, a freelance graphic designer, who accumulated $20,000 in credit card debt to help finance her business equipment and supplies. The competitive and unpredictable nature of freelance work made it difficult for her to keep up with this substantial financial burden. After several discussions, the credit card company agreed to a debt settlement where they forgave $15,000 of her total debt, allowing her to pay just $5,000.

This substantial debt cancellation meant Sarah received a Form 1099-C from her credit card company reporting the $15,000 as canceled debt. Ignoring this form or failing to understand its importance could have significant consequences on her tax situation. As per IRS rules, the $15,000 forgiven is considered taxable income, unless specific exceptions apply (such as insolvency). Therefore, the inclusion of this amount on her tax return is crucial.

Failing to report the canceled debt could lead to understating her annual income, which might result in penalties or an audit by the IRS. By including the canceled debt in her tax computations, she ensures compliance with the IRS tax reporting rules, preventing possible legal repercussions and helping her understand her tax liabilities more accurately.

Thus, the importance of Form 1099-C is highlighted in this scenario, as it plays a critical role in how individuals and businesses handle cancellations of debt and comply with federal tax requirements, ultimately influencing their financial and tax-dealing aspects significantly.

How do I file Form 1099-C?

Form 1099-C is typically filed by the creditor, not the debtor. If you are a creditor who has cancelled a debt of $600 or more, you need to complete Form 1099-C and send a copy to the IRS and to the debtor. You can obtain the form from the IRS website. Fill out the form using the instructions provided by the IRS, which includes details like the amount of the debt cancelled, the date of cancellation, and the debtor’s information.

After completing the form, send Copy A to the IRS by the end of February if filing by paper, or by the end of March if filing electronically. Give Copy B to the debtor by January 31, so they can report the information on their tax return. Ensure that your submission adheres to IRS filing requirements, including deadlines and proper form submission methods.

Are there any specific regulations or compliance requirements associated with Form 1099-C?

Yes, there are specific regulations and compliance requirements associated with Form 1099-C, Cancellation of Debt. Creditors who have cancelled a debt of $600 or more are required to issue this form not only to the debtor but also to the IRS. The form must include accurate details of the creditor and debtor, the amount of debt cancelled, the date of cancellation, and any interest that was included in the cancelled debt amount.

Additionally, it must specify whether the debtor was personally liable for the debt. This form plays a critical role in ensuring that forgiven debt is reported as income by the debtor, which affects their taxable income and tax liability. Creditors must send out Form 1099-C by January 31 of the year following the cancellation of the debt to both the debtor and the IRS to ensure compliance with federal tax laws and facilitate accurate tax reporting. Failure to issue this form when required can lead to penalties and interest charges for both the creditor and the debtor.

What resources are available for assistance in completing and submitting Form 1099-C (e.g., professional advice, official instructions)?

For assistance in completing and submitting Form 1099-C, debtors and creditors can rely on several resources. The IRS provides official instructions which are detailed and helpful for understanding how to correctly fill out and file the form. These instructions are available on the IRS website. Additionally, professional tax advisors, accountants, or tax preparation services can offer guidance and ensure that the form is completed accurately according to the latest tax laws and regulations.

Moreover, many tax software programs include support for Form 1099-C, guiding users through the process of entering the correct information and electronically filing the form if eligible. For specific scenarios or unusual cases, consulting a tax professional is recommended to address individual circumstances effectively.

What are some common errors to avoid when completing and submitting Form 1099-C?

Form 1099-C, “Cancellation of Debt,” is used to report debt cancellations by lenders, and there are several key errors to avoid when completing and submitting this form. Ensuring accuracy is crucial as it directly impacts the tax liability of the debtor. Here are some common mistakes:

- Incorrect Taxpayer Identification Numbers (TIN): Ensure both the creditor’s and debtor’s TINs (typically their Social Security numbers) are correctly reported. Errors can lead to misfiled returns and notices from the IRS.

- Failing to Report the Correct Date of Identifiable Event: The date of the identifiable event is crucial as it determines the tax year in which the debt cancellation should be reported. Incorrect dates can result in reporting in the wrong tax year.

- Incorrect Amount of Debt Canceled: The amount reported should only be the amount of debt forgiven. Sometimes, errors occur when the fair market value of any property returned to the lender is not correctly subtracted from the total debt.

- Not Including Interest or Penalties if Required: If the terms of the canceled debt include the cancellation of interest or penalties, these amounts should also be included unless separately stated.

- Misunderstanding the Exclusions and Exceptions: Not all canceled debts are taxable. For example, debts discharged in bankruptcy or qualified principal residence indebtedness might be eligible for exclusion. It’s a common error to fail to apply these rules when applicable.

- Failure to Send the Debtor a Copy of Form 1099-C: The debtor needs this form to report any potentially taxable income on their tax return. Failure to provide a copy can result in penalties.

- Issuing the Form When Not Required: Sometimes a Form 1099-C is issued when the debt has not actually been canceled, such as when it is only renegotiated or when collection has been paused but not formally forgiven.

- Using Incorrect Box Entries: Each box on the form serves a specific purpose, such as identifying the interest if included in the debt canceled or specifying if the debtor was personally liable. Misreporting these details can lead to confusion and incorrect tax filings.

- Omitting Insolvency Information: If the debtor was insolvent immediately before the debt was canceled, the amount up to the extent of insolvency may not be taxable. This requires careful calculation and documentation, which is often overlooked or mishandled.

- Not Retaining Copies: Creditors should keep copies of the 1099-C forms they issue for at least four years as proof of compliance and for reference in case of disputes or audits.

Avoiding these errors will help ensure that the Form 1099-C is completed and submitted accurately, helping both creditors and debtors handle their tax responsibilities appropriately.

How should you retain records or copies of the submitted Form 1099-C and associated documents?

It is important to retain a copy of Form 1099-C and any related documentation for at least seven years. This timeframe ensures that you can reference the documents if questions or issues arise from the IRS about the reported canceled debt. Keep these records in a secure location, whether in a digital format (ensuring files are backed up) or as physical copies in a fireproof and waterproof safe. Record-keeping should include all correspondence with the creditor regarding the cancellation of debt, along with any calculations or statements used to determine the amount of debt forgiven, which can be crucial for verifying the information on your tax return.

How do you stay informed about changes in regulations or requirements related to Form 1099-C?

Staying informed about changes in regulations or requirements related to Form 1099-C involves regularly checking updates from the Internal Revenue Service (IRS) on their official website. Additionally, subscribing to IRS newsletters and following relevant IRS social media channels can provide timely updates. Attending webinars, seminars, and continuing education courses offered by tax professionals or industry organizations can also be beneficial. Engaging with professional tax preparer forums and discussing changes with colleagues in the field are effective strategies to stay current on any modifications or clarifications regarding Form 1099-C.

Are there any exemptions or exceptions to the requirement of filing Form 1099-C?

Yes, there are exemptions and exceptions to the requirement of filing Form 1099-C. Entities are not required to file Form 1099-C for canceled debts that occur due to certain specific situations such as bankruptcy, insolvency, certain student loans discharged under specific provisions, and debts discharged during probate or similar proceedings. Additionally, certain business loans forgiven as a gift or bequest need not be reported. Also, creditors that are tax-exempt organizations typically do not need to file this form. Each exception or exemption involves specific qualifying conditions that must be met to avoid the reporting requirement.

Are there any penalties for inaccuracies or omissions on Form 1099-C?

Yes, there are penalties for inaccuracies or omissions on Form 1099-C. The IRS can impose penalties on the creditor for failing to file a correct form or for not providing accurate information. The penalty amount depends on how late the accurate information is provided and can range from $50 to $280 per form, with a maximum penalty depending on the size of the business and when the correct information is filed. Additionally, intentional disregard for filing or providing correct information can result in a minimum penalty of $570 per form, with no maximum cap.

How does Form 1099-C impact an individual or entity’s tax obligations?

Receipt of Form 1099-C indicates that a creditor has cancelled a debt of $600 or more, which generally requires the debtor to include the cancelled amount as taxable income on their federal tax return. This inclusion potentially increases the debtor’s overall tax liability for that fiscal year. Since the cancelled debt is treated as income, it could result in higher taxes owed to the IRS. To ensure compliance and accurate tax reporting, it is critical for individuals or entities to properly declare this income on their tax filings using the information provided on Form 1099-C. Failure to report this income could lead to penalties and interest charges from underreporting income for the tax year in question.

Is there a threshold for income or transactions that triggers the need to file Form 1099-C?

Yes, there is a threshold that triggers the need to file Form 1099-C. The creditor must file Form 1099-C if they cancel a debt owed to them of $600 or more.

Are there any circumstances where Form 1099-C may need to be amended after filing?

Yes, Form 1099-C may need to be amended after filing if there were errors in the initial filing such as:

- Incorrect debtor information

- Wrong amounts reported

- Missing details

Additionally, amendments might be necessary if the creditor subsequently recovers all or part of the debt after the cancellation was reported, or if there was a misinterpretation of the terms of the debt cancellation. In such cases, the creditor must issue a corrected Form 1099-C to both the debtor and the IRS to ensure accurate tax reporting.

How does Form 1099-C affect financial reporting for businesses, organizations, or individuals?

Form 1099-C impacts financial reporting primarily by affecting how income is recognized. When a business, organization, or individual receives a 1099-C form indicating that a debt was canceled, forgiven, or discharged, the amount specified as canceled debt on the form must be included as income on their tax return. This inclusion as income is necessitated because the Internal Revenue Service (IRS) treats forgiven debt as income that was previously not accounted for, thus potentially increasing the taxable income of the recipient.

For businesses and organizations, this can affect profit and loss statements as it introduces additional income that can affect the bottom line. This can also influence the tax liabilities of the entity or individual, leading to higher owed taxes if no applicable exceptions or exclusions apply. In summary, Form 1099-C requires that recipients reassess their financial accounting and tax reporting practices to ensure compliance and accuracy in their financial statements and tax filings.

Can Form 1099-C be filed on behalf of someone else, such as a tax preparer or accountant?

Yes, a tax preparer or accountant can file Form 1099-C on behalf of someone else as long as they have the authorization to do so. This often requires the taxpayer to provide the preparer with a power of attorney or another form of written consent allowing them to act on their behalf concerning tax matters.

Are there any fees associated with filing Form 1099-C?

There are no IRS fees associated with filing Form 1099-C. However, if a creditor uses a tax professional or software to prepare and file the form, they may incur costs related to those services.

How long does it typically take to process Form 1099-C once it’s been submitted?

Form 1099-C does not have a specific processing time once submitted by the creditor because it does not generally require action by the creditor beyond sending it to the IRS and the debtor. The debtor, who receives the form, must include the information from Form 1099-C when filing their tax return. The processing time would thus be dependent on the processing time of the debtor’s tax return. Tax returns, including the information from Form 1099-C, are typically processed by the IRS within 21 days if filed electronically, or six to eight weeks if filed by paper.

Can Form 1099-C be filed retroactively for past transactions or events?

Yes, Form 1099-C can be filed retroactively if a creditor failed to file it in the year the debt was actually canceled. This means if the debt cancellation was not reported in the appropriate tax year, the creditor can and should issue the form for past cancellations to ensure compliance with IRS requirements. However, this can lead to complications for the debtor who may need to amend past tax returns to account for the previously unreported income from the canceled debt.

Are there any specific instructions or guidelines for completing Form 1099-C for international transactions or entities?

Form 1099-C does not specifically address international transactions or foreign entities in its instructions, meaning there are no separate guidelines for handling cancellations of debt involving parties outside the United States. All creditors, whether domestic or international, who cancel a debt owed by a U.S. taxpayer must issue Form 1099-C if the debt cancellation meets the criteria (over $600). It is crucial for entities involved in international finance to consult with a tax professional to ensure compliance with both U.S. tax obligations and any applicable foreign tax laws. This ensures that the reporting on Form 1099-C aligns with international standards and that the necessary information is accurately conveyed to the IRS.

What digital tools or software are recommended for generating and managing Form 1099-C?

FormPros could be a suitable tool for generating and managing Form 1099-C, as we offer customizable templates and features designed to streamline the process. Additionally, popular accounting software such as QuickBooks or Xero often include features for generating and managing tax forms like the 1099-C. These tools can automate much of the process and help ensure compliance with tax regulations. However, it’s essential to review the specific features and capabilities of each tool to determine which best suits your needs.

Form 1099-C FAQs

-

What types of debt cancellation need to be reported on Form 1099-C?

Any cancellation of debt of $600 or more by a financial institution, credit union, federal government agency, or an organization having a significant trade or business of lending money must be reported on Form 1099-C. This includes personal loans, credit cards, mortgages, and car loans.

-

How does the IRS treat different forms of debt relief, such as mortgage forgiveness, in relation to Form 1099-C?

The IRS typically considers forgiven debt as taxable income. However, there are exceptions like the Mortgage Forgiveness Debt Relief Act, which may allow taxpayers to exclude forgiven mortgage debt from their income under certain circumstances, such as if the debt was forgiven in a foreclosure or mortgage restructuring.

-

If a debt is partially forgiven, how should it be reported on Form 1099-C?

Partial forgiveness of debt should still be reported on Form 1099-C. The form should reflect the amount of the debt forgiven, not the remaining balance.

-

What should a debtor do if they disagree with the amount listed on a received Form 1099-C?

If a debtor disagrees with the amount listed, they should first contact the creditor to resolve the discrepancy. If it cannot be resolved directly, they may need to consult a tax professional or attorney.

-

How does bankruptcy affect the filing and reporting requirements of Form 1099-C?

Debts discharged in bankruptcy are not considered taxable income. However, the creditor is still required to file Form 1099-C, indicating that the debt was discharged in bankruptcy in Box 6 with the identifiable event code "A."

-

Are non-profit organizations required to file Form 1099-C when they forgive a debt?

Yes, non-profit organizations are required to file Form 1099-C if they engage in a significant trade or business of lending money and they forgive a debt of $600 or more.

-

How can errors on a previously submitted Form 1099-C be corrected?

To correct an error on a previously filed Form 1099-C, the issuer must send a corrected form to the IRS and provide a copy to the debtor. The corrected form should be marked as "Corrected" at the top.

-

What are the implications of Form 1099-C on state tax filings?

The cancellation of debt reported on Form 1099-C may also be taxable at the state level. Debtors should check with their state's tax agency or a tax advisor to understand the specific implications for their state tax filings.

-

Is electronic filing of Form 1099-C accepted by the IRS, and if so, how can it be done?

Yes, the IRS accepts electronic filing of Form 1099-C, which is encouraged for entities submitting 250 or more forms. Electronic filing can be done through the IRS FIRE (Filing Information Returns Electronically) system. Filers need to apply for an account and follow the specific electronic filing requirements.

-

What privacy concerns should debtors have with the information provided on Form 1099-C?

Debtors should be aware that Form 1099-C includes sensitive personal information, such as their Social Security number and the amount of debt forgiven. It is important that this information is handled securely to prevent identity theft or data breaches. Creditors are required to comply with privacy laws and IRS regulations regarding the handling and sharing of personal information.