W-9 vs W-4 (2026): Key Differences for Employees and Contractors

With over 800 IRS tax forms in existence, it’s easy to mix things up (especially with the “W” series). Two of the most commonly confused are Forms W9 vs W4. Both collect your tax information, both go to someone at the start of a work relationship, and both carry IRS penalties if you ignore them. But each form targets a completely different type of worker and serves a completely different purpose.

Employees fill out the W-4 when they start a new job; it tells their employer how much income tax to withhold from each paycheck. Independent contractors fill out the W-9 to provide their Taxpayer Identification Number (TIN) to the businesses that pay them. If you work a traditional job, you need a W-4. If you work as a freelancer, consultant, or independent contractor, you need a W-9.

Table of Contents

W-9 vs W-4 at a Glance

| Form W-9 | Form W-4 | |

| Who fills it out | Independent contractors / self-employed workers | Employees (W-2 workers) |

| Purpose | Provides TIN to the hiring business for 1099-NEC reporting | Tells employer how much income tax to withhold from paycheck |

| Filed with the IRS? | No — kept by the hiring business | No — kept by the employer |

| When to submit | Before starting work / before the 1099 deadline (Jan 31) | On or before first day of employment |

| Tax withholding | None — contractor handles their own taxes | Employer withholds federal income tax per W-4 instructions |

| Related form | Form 1099-NEC (sent to contractor at year-end) | Form W-2 (sent to employee at year-end) |

| Current IRS form version | Rev. March 2024 | 2025 version |

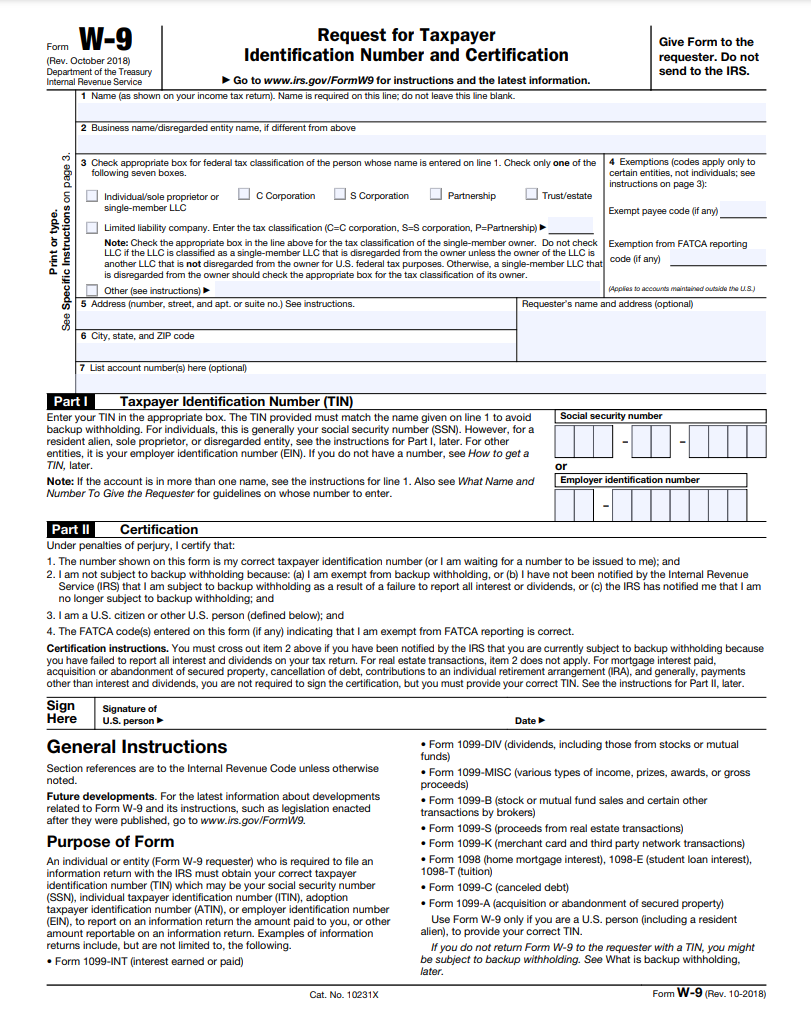

What is Form W-9?

Form W-9, officially titled the “Request for Taxpayer Identification Number and Certification,” is a one-page IRS form that businesses use to collect tax information from independent contractors before work begins. The company keeps it on file (never filing it with the IRS) and uses the information to prepare a Form 1099-NEC at year-end.

When a business pays an independent contractor $600 or more in a calendar year, it must report those payments to the IRS using Form 1099-NEC. To do that accurately, it needs the contractor’s name, address, and Taxpayer Identification Number (all of which come from the W-9).

Who is an Independent Contractor?

Independent contractors (also known as freelancers, consultants, or 1099 workers) are self-employed individuals who:

- Control when, where, and how they complete their work

- Do not receive employee benefits such as health insurance, paid leave, or 401(k) matching

- Are responsible for paying their own federal and state income taxes, including self-employment tax (15.3% on net earnings up to the Social Security wage base)

Common independent contractors include graphic designers, writers, IT consultants, landscapers, real estate agents, and repair professionals.

What Information Does a W-9 Collect?

A completed W-9 contains:

- Legal name (or business name)

- Federal tax classification: individual/sole proprietor, single-member LLC, C corporation, S corporation, partnership, trust/estate, or LLC treated as a corporation

- Mailing address

- Taxpayer Identification Number (TIN): either a Social Security Number (SSN) or Employer Identification Number (EIN)

- Certification signature confirming the TIN is correct and the contractor is not subject to backup withholding

Where Do You Submit a W-9?

Submit the W-9 directly to the company or individual hiring you, not to the IRS. The business keeps it in their records and uses the information when preparing the 1099-NEC. Most businesses request a W-9 before work begins or before making the first payment. Contractors who work with multiple clients may need to complete a separate W-9 for each one.

What Happens If a Contractor Refuses to Submit a W-9?

If an independent contractor fails to provide a W-9, the hiring business must begin backup withholding, which is holding back 24% of every payment and sending it directly to the IRS. The business will still issue a 1099-NEC and report the withheld amount in Box 4. This is true even if total payments are under $600.

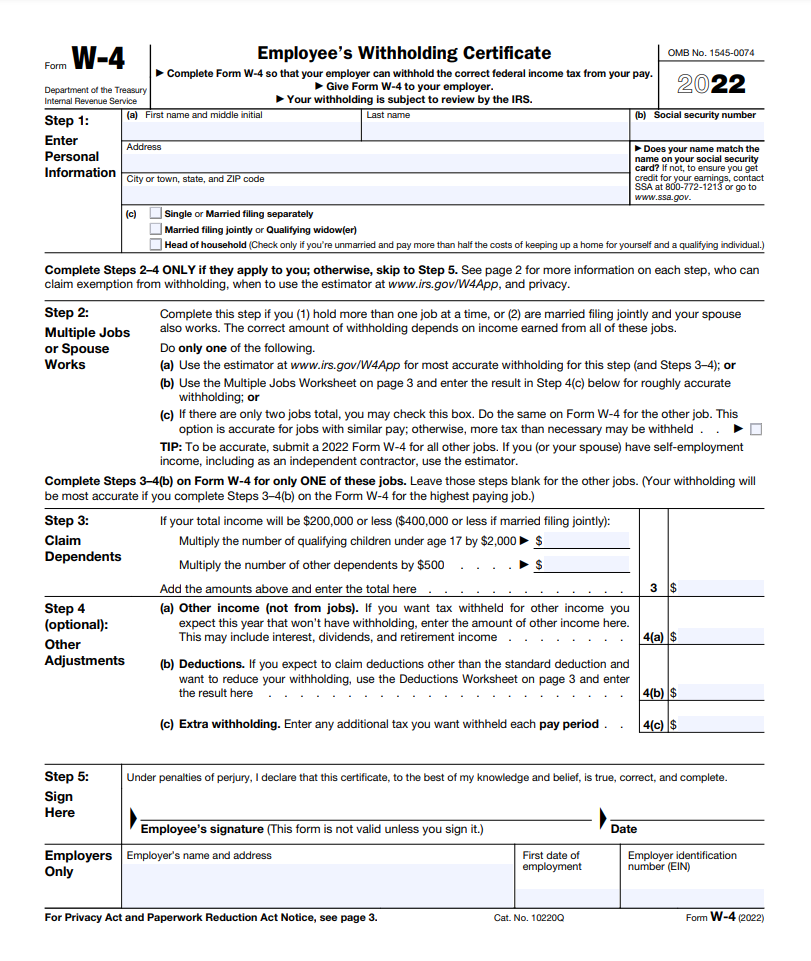

What is Form W-4?

Form W-4, “Employee’s Withholding Certificate,” is a federal form that employees complete when starting a new job. It tells the employer how much federal income tax to withhold from each paycheck. The IRS redesigned the W-4 in 2020 to eliminate the old withholding allowances system and replace it with a more straightforward calculation based on filing status, additional jobs, dependents, and other income.

Employers use the information on the W-4 (along with IRS Publication 15-T withholding tables) to calculate the correct amount of federal income tax to deduct from each paycheck. The employer then remits that withheld tax to the IRS on the employee’s behalf throughout the year.

Who Needs to Fill Out a W-4?

Anyone starting new employment as a W-2 employee must complete a W-4. This includes:

- New hires on their first day (or before their first paycheck)

- Existing employees who experience a change in tax situation: new marriage, divorce, a child, a second job, a major pay increase, or significant deductions

- Anyone who claims exemption from withholding (valid only if you had no tax liability last year and expect none this year)

What Information Does a W-4 Collect?

The current W-4 (2026) includes:

- Step 1: Name, address, Social Security number, and filing status (Single/MFS, Married filing jointly, or Head of household)

- Step 2: Multiple jobs adjustment (if you or your spouse have more than one job)

- Step 3: Claim dependents — child tax credit and other dependent credits

- Step 4 (optional): Other income not from jobs, deductions beyond standard, and any extra withholding amount per pay period

- Step 5: Signature and date

Steps 2 through 4 are optional for employees with a simple tax situation (one job, one income, no dependents). If left blank, the employer withholds at the default rate for the selected filing status.

What Happens if an Employee Doesn’t Submit a W-4?

Employers must still withhold federal income tax even without a W-4 on file. When no W-4 is on file, the IRS instructs employers to withhold at the Single/No Adjustments rate, which is the highest default rate. This typically withholds more tax than necessary, meaning a larger refund at filing time but less take-home pay throughout the year.

Key Differences Between W-9 and W-4

The most important distinction is the type of worker each form applies to. Everything else flows from there:

Employment Status Determines Which Form You Need

If you are an employee (meaning you receive a regular paycheck, your employer withholds taxes, and you receive a W-2 at year-end), you complete a W-4.

If you are an independent contractor (meaning you invoice clients, manage your own taxes, and receive a 1099-NEC at year-end), you complete a W-9.

This distinction matters because the IRS treats employees and contractors very differently for tax purposes. Employers must withhold federal income tax, Social Security tax, and Medicare tax for employees. They have no such obligation for contractors. The contractor pays the full self-employment tax (both the employer and employee portions) directly to the IRS.

Tax Withholding Works Differently

With a W-4, your employer withholds taxes automatically. You never see the money; your employer collects it and remits it to the IRS quarterly. At year-end, your W-2 shows what your employer withheld, and your tax return reconciles what you actually owe.

With a W-9, there is no withholding at all. You receive your full payment and are responsible for estimating and paying your own taxes throughout the year; typically through quarterly estimated tax payments to the IRS (using Form 1040-ES). If you underpay, you may face a penalty.

Neither Form Goes to the IRS

This surprises many people: both the W-4 and the W-9 are kept by whoever receives them. Your employer keeps your W-4 on file. The company you contract with keeps your W-9 on file. Neither form is submitted to the IRS directly. The IRS eventually gets the information through the downstream forms; your W-2 (for employees) or your 1099-NEC (for contractors).

What About the W-2? How It Fits In

Many people confuse all three “W” forms. Here’s how they connect:

| Employee Path | Contractor Path | |

| Start of work | Complete Form W-4 | Complete Form W-9 |

| During the year | Employer withholds taxes from each paycheck | Pay quarterly estimated taxes (Form 1040-ES) |

| Year-end form received | Form W-2 (Wage and Tax Statement) | Form 1099-NEC (Nonemployee Compensation) |

| Tax filing | File Form 1040, reconcile withholding | File Schedule C + Schedule SE with Form 1040 |

The W-2 is issued by employers to employees after year-end, reporting wages paid and taxes withheld. The 1099-NEC is issued by businesses to contractors after year-end, reporting nonemployee compensation paid.

Neither form requires action from the worker to generate. They are produced by whoever paid you.

Can You Need Both a W-9 and a W-4?

Yes and it’s more common than you’d think. If you hold a regular W-2 job and also do freelance or consulting work on the side, you will need:

- A W-4 for your primary employer

- A W-9 for each client that pays you $600 or more as a contractor

In this situation, your employer withholds taxes on your W-2 income, but you’re responsible for paying taxes on your freelance income separately. Many people in this situation increase their W-4 withholding (using Step 4(c) on the W-4) to cover their expected tax liability on freelance earnings, avoiding the need to make separate quarterly estimated payments.

If an employer gives you both a W-4 AND a W-9 and asks you to pick one, that’s a red flag. Workers are legally classified as either employees or independent contractors — this distinction has significant tax and legal implications, and misclassification can result in penalties for both parties. If you’re unsure how you’re classified, ask your employer or consult a tax professional.

FAQs

-

What is the main difference between a W-9 and a W-4?

The W-4 is for employees and controls how much income tax their employer withholds from each paycheck. The W-9 is for independent contractors and provides their TIN to the businesses that hire them for tax reporting purposes. The key difference is worker classification: employees use W-4, contractors use W-9.

-

Do I fill out a W-4 or W-9 as an independent contractor?

Independent contractors fill out a W-9, not a W-4. The W-9 gives your client the information they need to send you a 1099-NEC at year-end and report your earnings to the IRS. No tax is withheld from your payments; you're responsible for paying your own self-employment tax and income tax directly to the IRS.

-

What is the difference between W-2, W-4, and W-9?

These three forms serve different roles in the employment tax system. The W-4 is filled out by employees at the start of a job and sets their withholding. The W-9 is filled out by contractors and collects their TIN. The W-2 is issued by employers to employees after the year ends, summarizing wages paid and taxes withheld. The contractor equivalent of the W-2 is the 1099-NEC, which reports payments made to contractors.

-

Does a W-9 mean I'm an independent contractor?

Generally, yes. If someone asks you to fill out a W-9 instead of a W-4, they're treating you as an independent contractor. This means no taxes will be withheld from your pay, you'll receive a 1099-NEC instead of a W-2, and you're responsible for paying self-employment tax. If you believe you should be classified as an employee, you can ask the company to clarify your status or file IRS Form SS-8 to have the IRS determine your classification.

-

What happens if I refuse to fill out a W-9?

If you refuse to provide a W-9 or a valid TIN, the company paying you is required to withhold 24% of every payment (backup withholding) and send it to the IRS. They will still issue a 1099-NEC at year-end, reporting both your total pay and the amount withheld. You can reclaim the withheld tax when you file your return, but it's easier to simply provide the W-9.

-

What happens if I don't fill out a W-4?

If you don't submit a W-4, your employer will still withhold federal income tax. But at the default rate for Single with no adjustments, which is the highest default rate. This usually means more is withheld than you actually owe, resulting in a refund when you file but lower take-home pay throughout the year. It's always better to submit a completed W-4 so your withholding matches your actual tax situation.

-

Can a business ask for both a W-9 and a W-4?

No, these forms correspond to two mutually exclusive worker classifications. An employee fills out a W-4; a contractor fills out a W-9. If a business asks you to fill out both, that may indicate worker misclassification. This is a violation of IRS rules that can result in penalties for the employer. If this happens to you, seek clarification on your worker status.

-

When does a W-9 need to be submitted?

Independent contractors should submit a W-9 to each client before work begins or before receiving the first payment. The client needs it on file before the 1099-NEC deadline (January 31 each year. If January 31 falls on a weekend or holiday, the deadline moves to the next business day). If you don't have a W-9 on file, the client may delay payment or begin backup withholding.

-

Do self-employed people fill out a W-4 or W-9?

Self-employed individuals fill out a W-9 when they work for a client. They don't fill out a W-4 because no employer is withholding taxes on their behalf. Instead, they pay taxes directly to the IRS (usually through quarterly estimated payments) and report their business income on Schedule C when they file their annual tax return.