What is a Promissory Note?

A promissory note—also known as a loan agreement or an IOU—is a legal document that defines the details of a loan between two people.

This document clearly outlines the borrower’s promise to repay the lender in full within a specific amount of time. It provides a written record of the transaction and the borrower’s intentions.

Although it may seem like an informal document—particularly if you sign one when borrowing money from a friend or family member—these notes hold legal enforceability.

What is a Demand Promissory Note?

This variation of a regular promissory note requires the borrower to repay the loan when the lender demands payment. Once the lender notifies the borrower that they want their money, they specify a number of days for repayment.

What Types of Promissory Notes Are There?

- Informal or personal loans: One friend or family member lends money to another through this type of promissory note, often to cover expenses like a vehicle down payment or a student loan.

- Commercial: These notes define specific loan conditions in a formal agreement. Businesses often use them for financing.

- Real estate: This promissory note and deed of trust accompany a mortgage loan or other real estate purchase.

- Investment: A company issues a promissory note to raise capital, and investors can buy and sell these notes. Only savvy investors with the required resources should take on the risks associated with them.

Can a Promissory Note Be Handwritten?

Although a promissory note can be handwritten, writing it by hand is not advisable. Handwritten documents make it easier to add information later, even if both parties did not agree on the changes.

Using legally binding online tools like FormPros helps you avoid costly mistakes and potential legal issues caused by handwritten documents.

Why Do You Need a Promissory Note?

A promissory note generator formalizes a basic repayment agreement between two parties. This document defines the terms, dates, and amount of each payment due. Without one, you might not receive payment on time or could face other issues.

A promissory note can be either secured or unsecured:

- An unsecured promissory note relies solely on the maker’s ability to repay the loan.

- A secured promissory note ties the loan to an item of value, such as a house.

When Do You Need a Promissory Note?

Create a promissory note if you want a legally enforceable agreement that clearly defines the repayment terms. It also provides an official record of the repayment promise. Use a Promissory Note maker in the following situations:

- You’re lending money to a party and want a formal written agreement.

- You plan to borrow money and want to secure it with collateral.

- You plan to loan money and need a structured payment schedule or intend to charge interest.

- You plan to borrow money from friends or family and want to document your intent to repay.

Why is a Promissory Note important?

Promissory notes provide flexible options to easily obtain funds. Writing out the financial terms protects both the lender and the borrower.

This document serves as a legal record of the agreement and helps ensure that the borrower repays the money.

What Are the Main Things That Should Be Included in This Form?

Even if you’re just creating a simple promissory note, ensure that it contains all of the correct information. Below is a list of essential details to include in your promissory note form:

Information about the borrower and lender:

— Clearly identify both parties involved in the loan by listing the lender and the borrower. The borrower may be an individual or a corporation.

Payment dates:

— Specify when the first payment is due and how long the borrower has to make it.

End of promissory date:

— Specify when the promissory note’s time period concludes.

Payment plan:

— Establish a schedule that details how the borrower must repay the loan and how frequently (weekly, monthly, annually). Here are a few different payment options:

- Lump-sum payment: The borrower repays the entire loan amount in one payment.

- Due on demand: The borrower must repay the loan when the lender requests repayment.

- Installment: A specified payment schedule dictates how the borrower repays the loan.

Interest rate:

— The agreement should define the interest rate, if any. The interest rate appears as a percentage of the borrowed amount and accrues at a specified interval over the course of the promissory note’s term.

Loan amount and interest:

— Clearly state the total loan amount, including interest, and explain how it is compounded.

Collateral:

— Collateral secures repayment. It involves pledging something valuable to the lender as a guarantee. For example, real estate (such as a house) can serve as collateral for a mortgage.

Consequences of late payments:

— Specify what happens if the borrower fails to pay on time, including any late fees and penalties.

Transfer or selling permissions:

— Clarify whether the lender may transfer or sell the loan and under what conditions.

Amendments:

— Just like many contracts or agreements, amendments become enforceable only when both parties agree to modify the note’s terms.

Signatures:

— Once the note is completed, both parties must sign the agreement, officially binding its terms. Depending on their level of trust, they may also choose to have the signatures notarized.

Are Promissory Notes Legal Contracts?

Like common law contracts, a promissory document or letter serves as a legal instrument. However, for the document to be legally enforceable, it must meet certain conditions—such as an offer and the acceptance of that offer. A legal promissory document is tailored to the loan amount and repayment terms.

Additionally, the promissory note outlines the terms and conditions agreed upon by both parties. Once both parties agree to the loan conditions and sign the document, the promissory note fulfills all requirements for a legally binding contract.

Do I Need Witnesses to Sign the Promissory Document?

Generally speaking, there is no requirement for a witness or notary public to witness the signing of the promissory note. However, a witness or notary public might need to be present while you sign the promissory note if state-specific laws require it.

Even if it is not required, having an objective third party witness the signing of the note will be better evidence if you need to enforce the agreed-upon repayment of the note. Signing the note in the presence of a notary public is the best evidence that the borrower signed the document.

Reasons to Consider Not Using a Promissory Note

A promissory note generator may not always be your best option. Consider the following possible drawbacks:

- Unsecured loans typically carry higher interest rates.

- Lenders may require a more formal agreement before lending larger sums of money.

- Your business doesn’t have the cash flow to support debt financing.

- Promissory notes may still be considered a public securities offering.

- If you don’t pay the promissory note, the lender could buy your assets in bankruptcy for the amount of outstanding debt.

What are the Tax Implications of Promissory Notes?

Whenever interest is earned or paid, there will be income tax implications for both lenders and borrowers.

– Principal, Interest, and Basis –

Before we discuss the tax implications for lenders and borrowers it’s important that you understand the note’s principal, interest, and tax basis. The note’s principal simply refers to the amount of money loaned to the borrower. The interest is the amount of money the lender makes for loaning the money.

Additionally, all loans have a basis that refers to the purchase price and costs associated with acquiring the investment.

– Tax Implications for the Lender –

Income generated from a promissory note is taxable income and must be reported as such. The interest that the lender earned on the note would be considered as income.

However, if you lent the money in a personal capacity instead of through a business it must be reported on your income tax return.

It’s also important to note that if the income you generated was more than $1,500, it must be reported on Schedule B of Form 1040 or 1040A.

– Tax Implications for the Borrower –

Depending on whether the loan is used for personal or business purposes, it has different tax implications for the borrower. Unless the loan is used for a home loan under IRS regulations, the interest payments are not tax-deductible if used for personal purposes.

If the loan is used for a valid business purpose, it is possible to deduct interest repayments as business expenses under IRS regulations.

– Concessional Loans and Forgiveness –

If a loan is forgiven, the amount must be treated as income and reported by the borrower on their tax return. If the loan is set at an interest rate below that set by the IRS, it is possible to treat the foregone interest as income.

Steps to Follow When Making Use of a Promissory Note

Since a promissory note is a legally binding financial document, there are certain things you’ll need to do to comply with the law. Take the following steps when using a promissory note:

- Carry out financial due diligence to ensure you can repay the loan.

- Compare other funding options for lower-cost alternatives.

- Do not solicit a loan from outside sources without speaking to an attorney. This could be considered a public offering unless you meet the requirements of Regulation D, the JOBS Act, or another exemption.

- Carefully review the terms of the promissory note. Standard forms may not include important provisions, or may contradict your intent.

- Execute the agreement, and keep copies securely stored for your records.

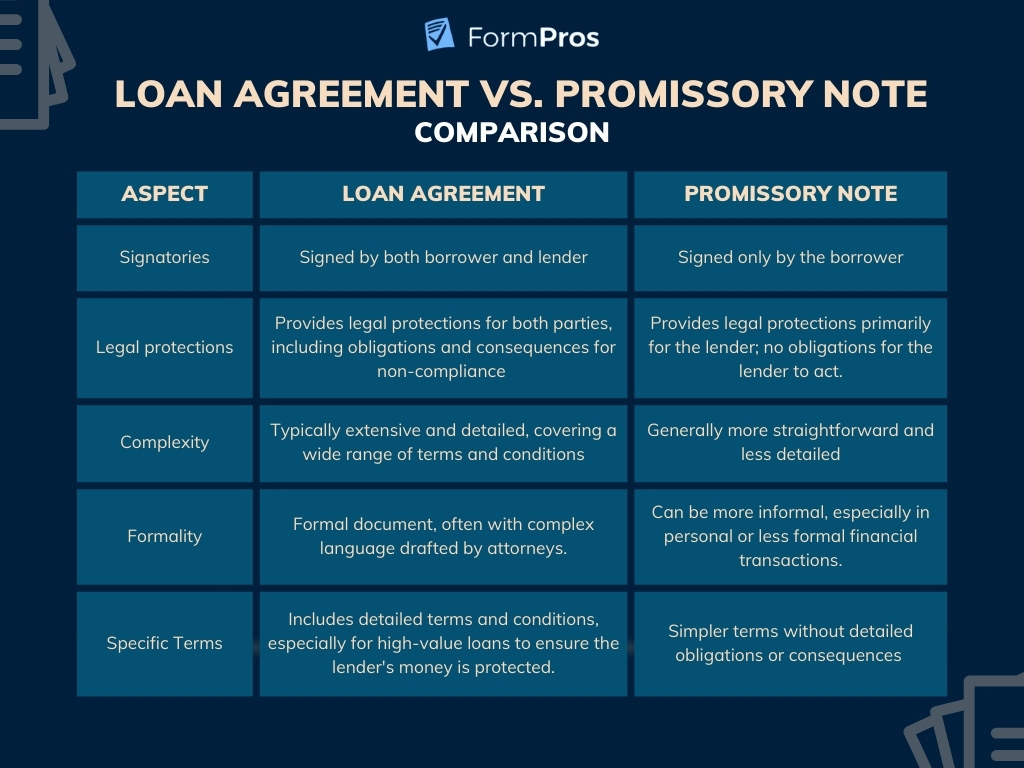

What’s the Difference Between a Promissory Note, an IOU, and a Loan Agreement?

The main difference is in the names, not the function. IOUs are generally less formal and may not have exact repayment terms.

Loan agreements – or loan contracts – are more formal and are often used by banks. Mortgages secure a loan with the title to real estate property. Let’s take a closer look at what each of these means.

What Is a Loan Contract?

The principles and main aim of a loan agreement and promissory document are similar because they both provide an agreement about the conditions of a loan repayment. However, the difference is that the loan agreement is more detailed than the promissory document.

Loan agreements are better to use when the principal amount of the loan is a large sum and the lender is unfamiliar with the borrower. A promissory document is a better option for smaller loans between trusted parties (such as family or friends).

What is an IOU?

An IOU is an acronym of the phrase, “I owe you” and consists of a document that acknowledges debt between two parties.

Whereas promissory notes are seen as legally binding, an IOU is an informal written agreement that states that one person owes another money.

Due to the informal nature of an IOU, a formal written agreement may follow because these documents can be difficult to enforce without stipulated conditions around the loan agreement.

What is a Mortgage?

A mortgage is a financial agreement made between a homeowner and a lender, with the promise to pay back the loan used to purchase real estate.

Similar to a promissory document, a mortgage outlines the repayment terms, the size of the loan, the interest rate, and the penalty for late fees. The difference between a mortgage and a promissory document is that the note is not entered into an official record.

What Are the Most Common Mistakes to Avoid When Creating a Promissory Note?

A promissory letter should be in a written format, not verbal. A note is only valid when it deals specifically with the exchange of money.

If you plan to include interest, it must be clearly stated in the document. You should also include the date on which the loan will “mature,” or be satisfied. Remember that the promissory note is not valid if it does not include both the signature of the borrower and the lender, so it is important to get it signed.

Here are some of the common mistakes:

- Not including all the necessary terms in the agreement.

- Not ensuring you have adequate cash flow to make timely payments.

- Violating covenants with other debt or equity holders that prohibit additional borrowing.

- Failing to protect your personal assets in case of default.

- Soliciting funds in a way that violates securities laws.

When Is a Promissory Note Void?

- If You Lose the Original: If you can’t prove the note ever existed, you have a problem. Suppose your debtor stops making payments, so you decide to sue for the money. When you gather your evidence, you can’t find the note, or even a copy of it. It’s still possible to collect—if you can prove that you own the note and that it’s been lost or destroyed. If the only evidence you have is your memory, you may be unable to prove your case. Different judges have taken different views of what constitutes proof of the debt. Even a copy of the original may not suffice because it’s easier to fake.

- If You Can’t Prove Ownership: Even if you can prove the note exists, you must show that you’re the legal owner. There are multiple mortgage cases where the mortgage note was transferred from one owner to the next, but the second owner never received it. Even if they paid to get the note, they never possessed it. The debt was out of reach.

- Flaws in the Note: Even if you have the original note, it may be void if it was not written correctly. If the person you’re trying to collect from didn’t sign it then the note is void. It may also become void if it fails some other law, for example, if it charged an illegally high interest rate.

What Happens When a Promissory Note Is Not Paid?

Someone who fails to repay a loan detailed in a promissory note can lose an asset that secures the loan, such as a home, or face other actions. You have a few options if someone who has borrowed money from you does not pay you back.

First, you should ask for the repayment in writing. A written reminder might be all you need to do to get your money paid back. Late fees reminders are commonly sent at 30, 60, and 90 days after the stated due date. If the borrower still does not pay you back, you might consider asking your borrower to make a partial payment. You can create a debt settlement agreement if you decide to accept partial repayment of a debt.

Another option to consider is creating an extended payment plan. This allows the borrower to pay you back in full over a revised period of time. You can also choose to use a debt collector to obtain repayment. A debt collector works with you to collect the note, generally taking a percentage of the payment.

Alternatively, you can sell the note to a debt collector. Selling a note to a debt collector gives the debt collector ownership of the loan and the ability to collect the full amount.

If nothing else works, you can also sue your borrower for the full amount owed to you.

Do I Need to Use a Law Firm, Accountant, or Notary to Help Me?

You can easily create a promissory note without hiring a lawyer, accountant, or notary.

Creating the form online with legally binding tools like FormPros can save you time and money. It can also cut out the hefty expense of hiring a lawyer.

Why Use FormPros’ Promissory Note Generator?

Our easy-to-use free online promissory note template generator was created by a staff of lawyers and business experts, and creates promissory notes for a fraction of the cost you would pay an attorney.

Our tool also has a subscription plan so you can create unlimited promissory notes at a low cost.

Here’s how to create your own promissory note in three simple steps with FormPros:

- Step 1: Answer a few simple questions to create your document.

- Step 2: Preview our promissory note templates to see how your document will look and make any edits.

- Step 3: Download your document instantly to your computer and then print or share it with the lender or borrower.

FormPros Has You Covered

Simplify your paperwork with FormPros! From creating paystubs, W-2s, and 1099-NEC forms to generating LLC Operating Agreements and even voided checks, our easy-to-use platform has you covered. Save time, reduce errors, and handle your business documents with confidence. Start now and see how FormPros makes professional form generation fast, affordable, and hassle-free!

Promissory Note FAQs

-

Can a promissory note be modified after it is signed?

Yes, but both parties must agree to any modifications. Changes should be documented in writing and signed by both the borrower and lender to remain legally enforceable.

-

What happens if a borrower wants to pay off the loan early?

Early repayment is generally allowed, but some promissory notes include prepayment penalties. Review the terms to see if any additional fees apply for paying off the loan ahead of schedule.

-

Do promissory notes expire?

Yes, promissory notes have a statute of limitations that varies by state. If the lender does not take action within this time frame, they may lose the right to collect the debt.

-

Can a promissory note be used for non-monetary loans?

Typically, promissory notes are used for financial loans. If you're lending property, goods, or services, a different type of contract, such as a loan agreement, may be more appropriate.

-

What if the borrower moves to another state?

The lender can still enforce the promissory note, but the legal process may change depending on the jurisdiction. It may be necessary to file in the new state’s courts for legal action.

-

Can a promissory note include a co-signer?

Yes, a co-signer can be added to provide additional security for the lender. If the borrower defaults, the co-signer becomes responsible for repaying the loan.

-

How does bankruptcy affect a promissory note?

If the borrower files for bankruptcy, the loan may be discharged, meaning the lender might not be able to collect. However, secured loans with collateral may still be recoverable.

-

What is the difference between a secured promissory note and a personal guarantee?

A secured promissory note ties repayment to a specific asset (like a car or house). A personal guarantee makes an individual personally responsible for repaying the loan, regardless of assets.

-

Can a promissory note be transferred to someone else?

Yes, lenders can assign or sell a promissory note to a third party. This means another entity could take over the collection of the debt under the same terms.

-

What should I do if the borrower claims they never signed the note?

If a borrower disputes signing the note, the lender may need to provide proof, such as witness statements or notarization. Having a notary verify the signatures can prevent these disputes.