Differences Between Payday, Pay Period And Pay Cycle

A pay period is the stretch of time you’re being paid for (say, two weeks of work); a payday is the date you actually receive that money; and a pay cycle is how often the whole thing repeats (weekly, bi-weekly, semi-monthly, or monthly). Employers, workers, and independent contractors all need to understand these three payroll terms to manage pay accurately and read a paystub correctly.

In this article, we define each term, compare the most common pay schedules (including bi-weekly vs. semi-monthly), explain what appears on a paystub, and walk through a real payroll calculation.

Table of Contents

Key Takeaways

- A pay period is the timeframe your paycheck covers; a payday is the date you’re paid; a pay cycle (or pay frequency) is how often paydays occur.

- The four common pay frequencies are weekly (52 paychecks/year), bi-weekly (26), semi-monthly (24), and monthly (12).

- Bi-weekly and semi-monthly are the most often confused: bi-weekly pays every two weeks (26 checks), while semi-monthly pays twice a month on fixed dates (24 checks).

- Your pay period — not your payday — determines the earnings, tax withholdings, and deductions shown on each paystub.

- You can generate accurate paystubs for any pay schedule with FormPros.

Understanding the Definitions Associated with Pay Period

Understanding how your pay stub displays income and tax withholdings starts with learning three key terms: payday, pay period, and pay cycle. These terms define when and how you receive your wages and clarify what timeframe your paycheck covers.

– Payday –

A payday is the specific date on which employees or independent contractors receive their wages. It is the day an employer issues payments, either through direct deposit, paper check, or payroll card.

For instance, if a company uses a biweekly pay schedule and pays employees every two weeks, April paydays might fall on April 5th and April 19th. On the other hand, if the company follows a semimonthly schedule (twice a month), paydays could be on April 15th and April 30th.

Ultimately, payday is crucial for budgeting because it determines when employees receive their earnings and when employers process tax deductions.

– Pay Period –

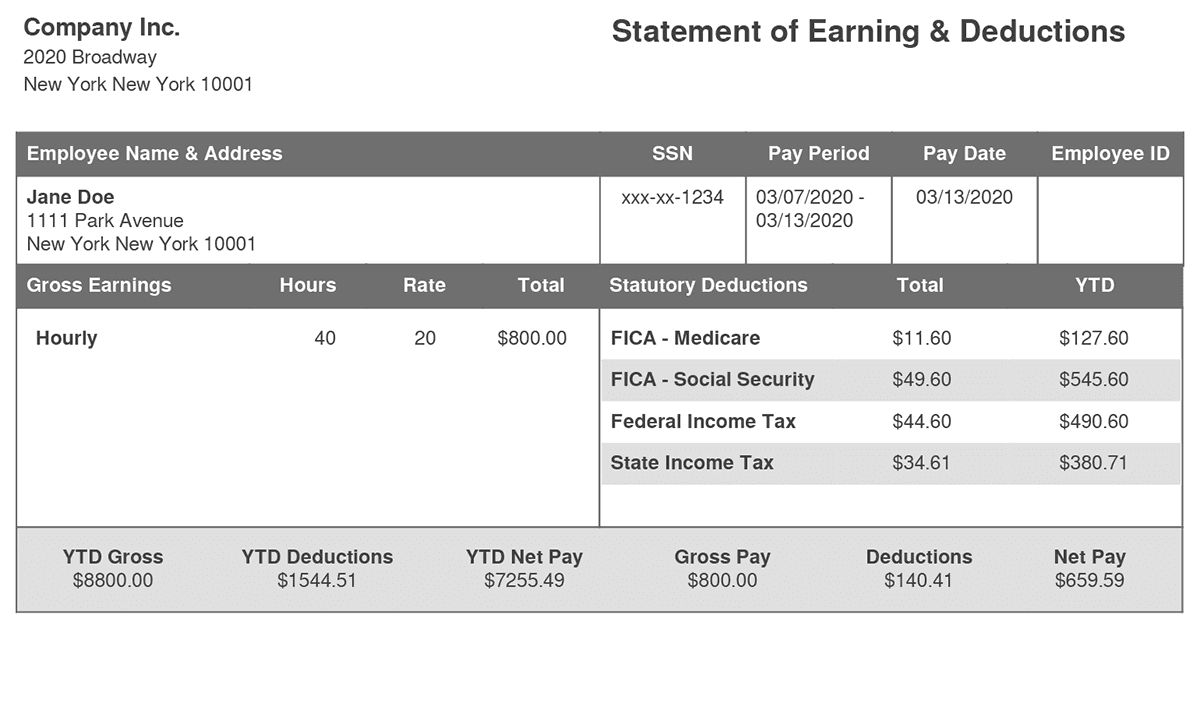

A pay period is the timeframe a paycheck covers — it starts on one date and ends on another, covering the work performed or hours logged during that span. Depending on the employer’s pay cycle, the length of a pay period can vary.

For example, using the biweekly pay schedule mentioned earlier, a company paying employees on April 5th would have a pay period covering March 22nd to April 4th. Then, the next pay period would be April 5th to April 18th, with payday falling on April 19th.

For semimonthly pay, the two pay periods for April could be April 1st to April 15th and April 16th to April 30th. Although both biweekly and semimonthly schedules typically result in two paychecks per month, their pay periods don’t always align because the structure of each month varies.

Understanding the pay period matters because your paycheck’s earnings, tax deductions, and benefits contributions all apply specifically to this timeframe; not to the payday on which you’re paid.

– Pay Cycle –

A pay cycle outlines the company’s payroll structure—how often the company pays employees and processes payroll calculations. (You’ll also hear this called pay frequency.) Company policy sets this structure, which may vary based on industry standards, employee classification (hourly vs salaried), and regulatory requirements.

Common Pay Frequencies Compared

Most employers use one of four pay frequencies. The one they choose determines how many paychecks you receive each year and how large each one is for the same annual salary.

| Pay Frequency | How Often | Paychecks/Year | Commonly Used For |

|---|---|---|---|

| Weekly | Every 7 days (e.g., every Friday) | 52 | Construction, retail, gig work |

| Bi-weekly | Every 2 weeks (same weekday) | 26 | Corporate, healthcare, hourly staff |

| Semi-monthly | Twice a month (fixed dates) | 24 | Salaried employees |

| Monthly | Once a month | 12 | Executives; some small firms |

Understanding your pay frequency helps you plan your finances, since it shows how often you receive wages and how taxes and deductions are spread across the year.

Bi-Weekly vs. Semi-Monthly Pay: A Closer Look

Bi-weekly and semi-monthly are the two schedules people most often confuse, because both produce roughly two paychecks a month. The difference is in the count, the size, and the timing:

- Bi-weekly pays every two weeks on the same weekday (e.g., every other Friday), producing 26 paychecks a year — which means two months each year contain three paydays.

- Semi-monthly pays twice a month on fixed calendar dates (e.g., the 15th and the last day), producing exactly 24 paychecks a year, always two per month.

Because bi-weekly splits the year into 26 checks instead of 24, each bi-weekly paycheck is slightly smaller than a semi-monthly one for the same annual salary — but you receive two extra checks per year. Semi-monthly paydays are more predictable by date, while bi-weekly paydays always fall on the same weekday.

| Bi-Weekly | Semi-Monthly | |

|---|---|---|

| Paychecks/year | 26 | 24 |

| Timing | Every 2 weeks (same weekday) | Twice a month (fixed dates) |

| Paycheck size | Slightly smaller | Slightly larger |

| Best suited to | Hourly staff and overtime | Salaried staff |

| Watch-outs | Two months have three paydays | Paydays may land on weekends/holidays |

For employers, bi-weekly tends to be simpler for hourly and overtime calculations because it lines up with the weekly workweek, while semi-monthly maps cleanly onto monthly accounting and salaried payroll. Switching between them doesn’t change anyone’s annual salary (only the size and timing of each check) but it does require clear communication to avoid confusion.

Why These Terms Matter

A pay stub breaks down an employee’s earnings, tax withholdings, and deductions based on these terms. When reviewing a pay stub, it’s especially important to distinguish between:

- Current Amounts – Earnings and deductions for the most recent pay period.

- Year-to-Date (YTD) Amounts – Cumulative earnings and deductions from the beginning of the year up to the current paycheck.

By having a clear understanding of the differences between payday, pay period, and pay cycle, employees and independent contractors can better manage their finances, anticipate deductions, and ensure they are paid correctly.

Specific Information on a Pay Stub

Employers provide this information to each employee and contractor:

— Payroll Cycle: The number of pay periods determines how much salary is paid on each payroll date. Additionally, it determines the start and ending days for computing hourly payroll.

— Wages: Gross pay and net pay. Wages may be based on a salary, or calculated using an hourly rate of pay.

— Tax Withholdings: Federal, state, and possibly local amounts withheld for taxes.

— Benefit Withholdings: Amounts withheld for the employee’s share of insurance premiums, or funds to be invested in a retirement plan.

As a result, every business must collect data to calculate gross wages and net pay. However, if you employ independent contractors, you don’t need to withhold taxes from pay.

Calculating Net Pay

Here are the details you need to calculate net pay. (For a full step-by-step walkthrough, including overtime, see our guide on how to calculate wages.)

1) Gross Wages

Wages earned before any withholdings or deductions are subtracted. Gross wages for a pay period amount are calculated in one of two ways:

- Salaried Employees: (Annual salary / number of pay periods in a year)

- Hourly Employees: (Hours worked X pay rate per hour)

Gross wages may include additional compensation, including sick pay, holiday pay, or bonuses.

2) Hours Worked and Pay Rate

The hours worked total is especially important for non-exempt (hourly) workers. The pay stub should include regular hours (up to 40 hours per week) as well as overtime hours.

The paystub must detail all hours worked, and the rate of pay earned for each hour. Some workers, including those covered by union contracts, must be paid a specific rate of pay for overtime or double-time hours.

*Salaried workers may also see hours listed on their pay stubs.*

3) Tax Deductions

Workers determine their federal income tax withholdings amounts by completing Form W-4, and each state has a tax withholding form.

Social Security Tax:

- Employee Contribution: 6.2% of earnings, up to a wage base limit of $184,500. This means the maximum Social Security tax an employee will pay in 2026 is $11,439.00.

- Employer Contribution: Employers match this 6.2% rate, contributing an equal amount for each employee.

Medicare Tax:

- Employee Contribution: 1.45% of all wages, with no wage base limit.

- Employer Contribution: Employers also contribute 1.45% of all employee wages.

- Additional Medicare Tax: Employees earning over $200,000 annually are subject to an additional 0.9% Medicare tax on earnings above this threshold. Employers are required to withhold this additional tax but do not match it.

In total, for employees earning up to $184,500, the combined FICA tax rate is 7.65% (6.2% for Social Security and 1.45% for Medicare). Employers also pay a combined rate of 7.65%, which is deductible as a business expense.

Example Payroll Calculation

Sally’s annual income is $60,000, and her firm processes payroll 26 times a year. Sally’s gross wages each pay period total ($60,000 / 26), or $2,308 per pay period.

Based on the allowances on her W-4, her company withholds 20% of her gross pay ($462) for federal taxes, and 5% ($115) for state taxes. Sally also pays $50 each pay period for her share of the company health insurance plan.

Sally’s net pay is $2,308, less a total of $577 for taxes and $50 for her health insurance premiums. Her net pay is $1,681.

The pay stub must include all of this information for the current payroll period and year-to-date. Hourly workers also need details about their total hours worked and any hours paid as overtime.

Employers need to generate accurate pay stubs, and thankfully, technology can help.

Take Charge of the Process

FormPros provides a pay stub generator that is not only user-friendly but also helps you produce accurate pay stubs in less time—for weekly, bi-weekly, semi-monthly, or monthly schedules. Use FormPros to take charge of the pay stub process.

FormPros Has You Covered

Simplify your paperwork with FormPros! From creating paystubs, W-2s, and 1099-NEC forms to generating LLC Operating Agreements and even voided checks, our easy-to-use platform has you covered. Save time, reduce errors, and handle your business documents with confidence!

FAQs

-

What is a pay period?

A pay period is the span of time a paycheck covers — the days you actually worked or were employed for that check. It's different from your payday (the date you're paid) and your pay cycle (how often you're paid). Earnings, taxes, and deductions on each stub apply to the pay period, not the payday.

-

Is bi-weekly or semi-monthly better?

Neither is universally better; they suit different needs. Bi-weekly (26 checks) lines up with weekly workweeks and is convenient for hourly and overtime pay. Semi-monthly (24 checks) maps neatly onto monthly accounting and salaried staff. Your annual pay is the same either way; only the size and timing of each check changes.

-

Can employers offer different pay cycles to different employees?

Yes, employers can offer different pay cycles based on factors like job classification (salaried vs. hourly), department, or location—as long as it complies with state labor laws and employment agreements. Consistency within the same job type is generally encouraged to avoid confusion and payroll errors.

-

Do independent contractors ever receive paystubs?

Although not legally required, some businesses voluntarily provide pay stubs to independent contractors for record-keeping. These stubs can help contractors track income, especially when filing taxes or applying for loans. Tools like FormPros make it easy for contractors to create their own.

-

What happens if a payday falls on a weekend or holiday?

If a scheduled payday falls on a weekend or federal holiday, employers typically process payroll one business day earlier. This ensures employees receive wages on time. Always consult your state's labor laws, as some require early disbursement.

-

How does switching from biweekly to semimonthly affect employee pay?

Switching pay cycles doesn't change an employee's annual salary, but it alters paycheck amounts and timing. Semimonthly checks are slightly larger but occur less frequently. Such transitions require clear communication and planning to avoid confusion.

-

Are digital pay stubs legally valid?

Yes, digital paystubs are legally valid in most states, provided employees can access and print them. Some states require employees to opt in or be given paper copies, so verify local regulations before going paperless.

-

What payroll records must employers keep, and for how long?

Employers are generally required to retain payroll records—employee hours, wages, tax withholdings, and pay stub details—for at least three years under the Fair Labor Standards Act. Some states or regulatory bodies may require longer.

-

How are bonuses and commissions reflected on pay stubs?

Bonuses and commissions typically appear as separate line items, often labeled "supplemental income." These amounts are subject to withholding, sometimes at a flat supplemental rate. Clear labeling helps employees understand the origin of additional earnings.