New Schedule 1-A Tax Form: What It Is and Who Needs to File It

The OBBBA created Schedule 1-A, a brand-new IRS form for claiming deductions on tips, overtime, car loan interest, and an enhanced senior deduction.

The OBBBA created Schedule 1-A, a brand-new IRS form for claiming deductions on tips, overtime, car loan interest, and an enhanced senior deduction.

The OBBBA raises the 1099-NEC and 1099-MISC reporting threshold from $600 to $2,000 starting in 2026, while the 1099-K threshold reverts to $20,000 and 200 transactions.

Skip the guesswork. Learn how to estimate your 2025 federal tax withholding fast so you can stay on track and avoid surprises at tax time.

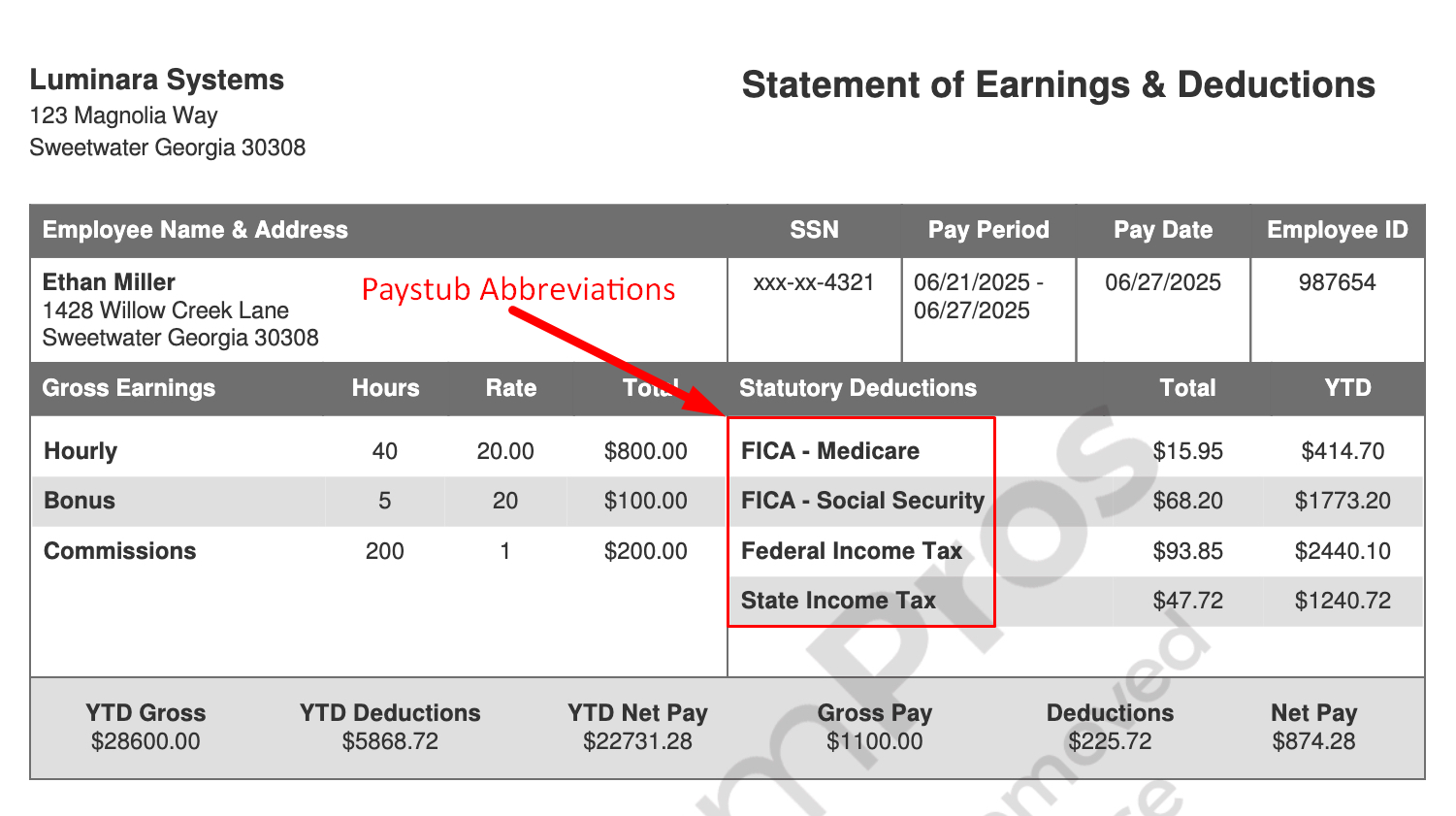

Confused by paystub abbreviations? This quick guide breaks down every code so you can read your paycheck with confidence.

If you’re self-employed, you can still prove your income. Here’s how to make accurate, legal paystubs that lenders will actually accept.

Learn the key differences between Forms 1099-NEC and 1099-MISC, who needs each one, and how to file them correctly before deadlines.

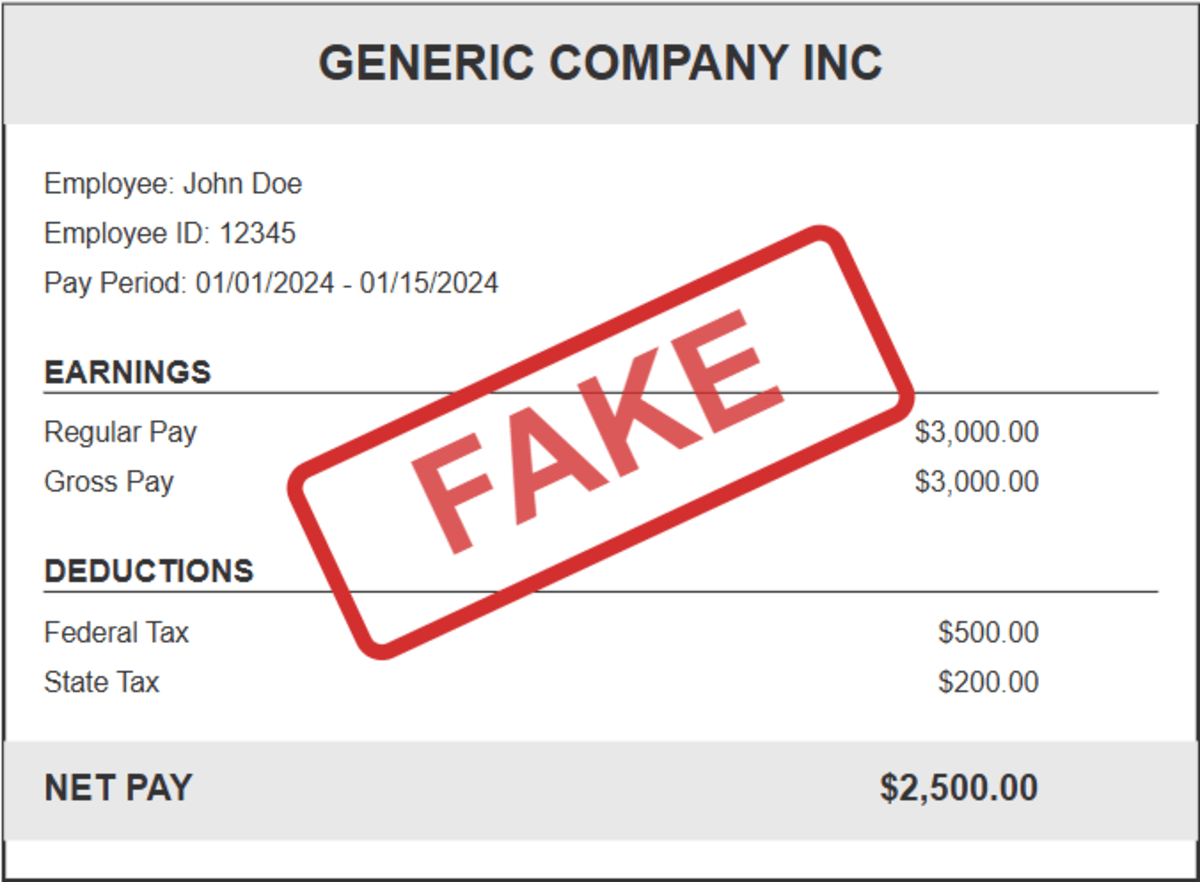

Fake paystubs are easier to spot than you think. Look for bad math, round numbers, and missing employer details.

Wondering if your employer has to give you a paystub? It depends on your state — here’s how to find out, what your rights are, and what to do if you can’t get one.

Worked more than 40 hours? Here’s how to calculate your overtime pay — plus a paystub calculator to double-check your earnings.

Sometimes — but it’s risky. You can technically file taxes using your final paystub, but it’s not recommended. The IRS prefers an official W2, and filing without one can cause delays, errors, or even rejections. When It’s Possible You may be able to file taxes with your last paystub if your employer hasn’t sent your […]